[ad_1]

Getty Images/iStockphoto

The last few years have provided a challenging landscape for prospective homeowners and those looking to refinance their mortgages. Many would-be borrowers have sat on the sidelines as elevated home prices and high mortgage rates have made financing options less affordable.

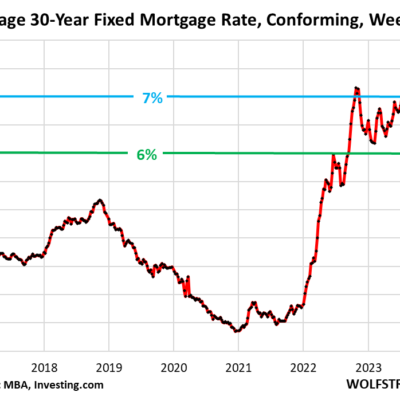

Fortunately, the housing market is beginning to show positive signs, such as mortgage rates dropping to a four-month low in July. According to Freddie Mac data, the average mortgage rate on a 30-year fixed-rate mortgage is 6.73%, around a point lower than it was toward the end of 2023.

With mortgage rates dropping, then, it may be wise to consider locking in a mortgage rate now, depending on how rates are expected to move in the future. We asked some experts for their suggestions, broken down below.

See how low of a mortgage rate you could lock in here now.

Should you lock in a mortgage interest rate this August?

With mortgage rates experiencing a modest drop, should you lock in a mortgage rate now or wait? Brian Shahwan, vice president at William Raveis Mortgage, suggests “floating the rate” may be a savvy move to consider if rates continue to fall. Floating the rate is when you delay locking in a rate with your lender in the hope rates will drop further before closing your loan.

Shahwan notes that the decision to lock in a rate now or wait depends on your specific situation and where you are in the loan process. “With rates improving week over week, it is my recommendation to float the rate as long as possible and lock in a dip in the market. Banks typically want the rate locked in around seven to 10 days from closing, so as long as the loan officer has a good pulse on the market, it can be very beneficial for the borrower to float as long as possible.”

If you’re waiting for rates to drop before locking in, you may only see modest short-term changes, perhaps not enough to move the needle in terms of significant savings. “The rest of the year will likely hold the range we’ve had since early spring of mid to upper 6% for the average 30-year fixed-rate,” says Afifa Saburi, a capital markets analyst at Veterans United Home Loans. “There isn’t much room for rates to fall lower, given we only have three Fed meetings for the remainder of the year after July. Rates are also unlikely to rise above the highs we saw this year in May because we have enough data to support a cut in the last quarter of the year.”

Start exploring your current mortgage rate options online now to learn more.

Another consideration

Many homebuyers are weighing their decision to lock in a rate against the likelihood of higher competition and prices if mortgage rates drop. Low inventory has strained the housing market in recent years, reaching a record low in January 2022. While inventory has grown since then, it still falls short of the demand for houses.

Remember, locking in a mortgage rate isn’t just about securing a great rate but also about positioning yourself well in a competitive housing market. In that case, locking in a rate and purchasing a home now may make sense, even if mortgage rates drop in the coming months.

Ryan Gordon, CEO/Senior Loan Officer at G Mortgage, observes, “As crazy as it sounds, a higher rate is helpful to homebuyers. Buy now before everyone on the sidelines breaks loose and creates so much competition that you’ll be paying more for your house.”

How should you shop for a mortgage loan now?

Projections for a Federal Reserve rate cut are injecting hope into the mortgage sector, but persistent inflation has been unhelpful for many borrowers. The recent drop in mortgage rates is a positive sign, so it may be wise to create a strategy if you’re shopping for a mortgage. Specifically, you should:

- Be ready to move. If you plan on buying a home soon, start working with a lender to get preapproved. This way, you’ll be ready to act quickly when the right home hits the market. If you wait to start the process, the seller might sell to a more prepared buyer.

- Get loan estimates from multiple lenders. The Consumer Financial Protection Bureau (CFPB) advises getting loan estimates from multiple lenders to find the best terms for you. Rates vary from one to another, so you may find significantly lower rates by shopping around. It’s always possible to negotiate with your mortgage lender, but the process is much easier when you have several quotes from different lenders. You can use these competing offers to negotiate a better mortgage rate and terms.

You can get loan estimates from multiple lenders online now.

The bottom line

“Timing the market” may be a fool’s errand since no one knows with absolute certainty what will happen with mortgage rates. Also, mortgage and real estate experts often advise homebuyers to “marry the house but date the rate.” That’s a clever way of saying to focus on finding a home that best suits your needs while realizing you can always refinance if rates drop in the future.

If you decide to lock in a rate now, shop and compare multiple lenders to find the best rate and terms available. Also, follow proven strategies to lower your mortgage rate, regardless of what the market does.

[ad_2]

Source link