The Bank’s Monetary Policy Committee decided to keep the base rate at 4.25 per cent following high inflation and geopolitical tensions

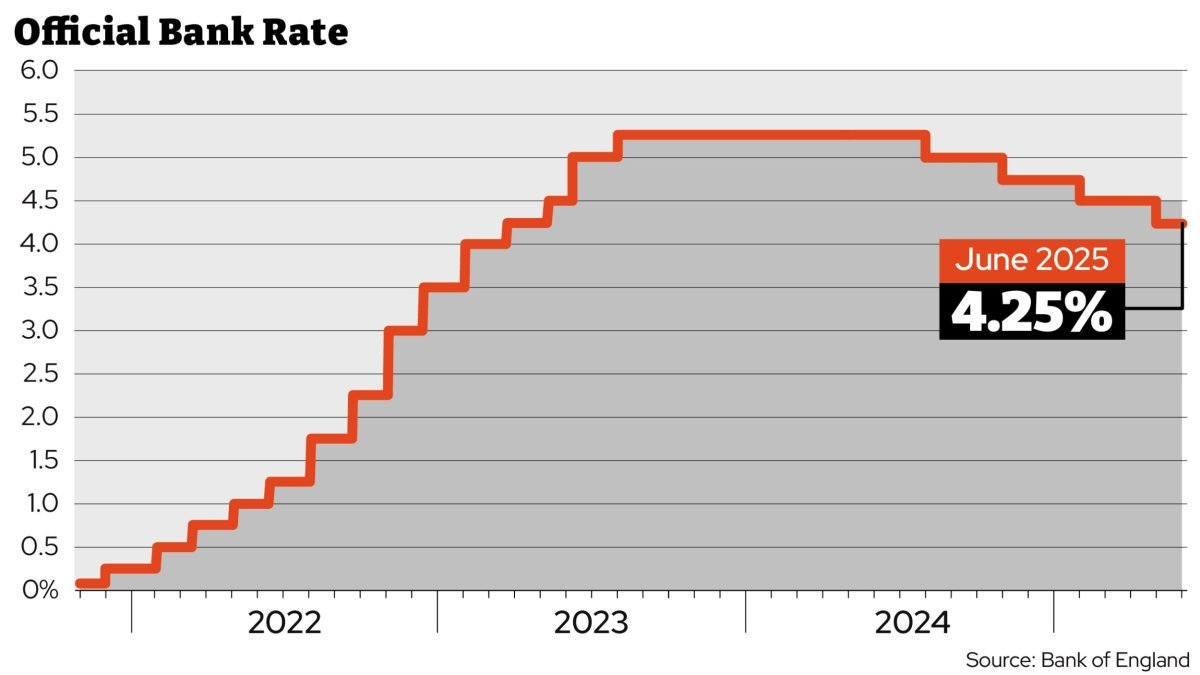

The Bank of England has held interest rates at their current level of 4.25 per cent, as was widely predicted.

The Bank’s Monetary Policy Committee (MPC) voted 6-3 in favour of holding the bank rate where it is, after previously cutting from 4.5 per cent in May.

Three members preferred to reduce the rate by 0.25 percentage points, to 4 per cent.

The Bank said it was keeping watch on a “highly unpredictable” world as it tries to balance high inflation, geopolitical tensions and a slowing economy.

Andrew Bailey, the Bank’s governor, said: “Interest rates remain on a gradual downward path, although we’ve left them on hold today. The world is highly unpredictable.”

He added that there were “signs of softening in the labour market” – referring to indicators including slower hiring and wage growth easing – which were being closely watched to see how far they feed into UK inflation.

It comes a day after May’s inflation figure was announced as 3.4 per cent – the same rate as April. This is well above the Bank’s target of two per cent.

What will happen to inflation?

The Bank of England expects inflation to remain broadly around 3.4 per cent throughout the remainder of the year before falling back towards target next year.

Paul Dales of Capital Economics expects the figure to be between 3 and 3.5 per cent for the rest of the year.

Oher economists expect it could be higher. Raj Badiani, of S&P Global Market Intelligence, said he expects a rise rise to 3.7 per cent in June.

Robert Wood, chief UK economist at Pantheon Macroeconomics, said: “Events in the Middle East driving up oil prices last week are a reminder of just how close to the wind the MPC is sailing.

“Oil and natural gas price gains last Friday, if sustained, would add 6 basis points to our average CPI inflation forecast between May 2025 and April 2026. The peak would nudge up to 3.7 per cent in September, from 3.6 per cent.”

Will interest rates be cut again this year?

It is widely expected that there will be at least one more interest rate cut this year, if not two.

Traders expect the next cut to come in August when the MPC meets again.

The Bank said in a note that “a gradual and careful approach to the further withdrawal of monetary policy restraint remains appropriate” given high inflation and global uncertainty.

How will the interest rate hold affect mortgage holders?

Those on variable-rate mortgages will not see a change to their repayments as a result of the hold.

Around four in five mortgage holders are on fixed-rate mortgages, where the interest rate is locked for a set period of time, which means that if you are on this type of loan, your repayments will also not change.

Instead, you will notice a change when your mortgage comes up for renewal.

Nick Mendes of John Charcol brokers said: “Whether the Bank had held interest rates steady or opted for a small cut, the outlook for mortgage holders in 2025 remains finely balanced.

“Inflation is easing, the labour market is cooling, and growth has slowed, but uncertainty around global risks and sticky services inflation means the rate path is still anything but settled.

“Even in a falling rate environment, borrowers would be wise not to wait passively. If your current fixed deal is due to end this year, it’s worth reviewing your options early, as some lenders allow new deals to be secured up to six months in advance.”

The average rate on a two-year fixed mortgage is 5.11 per cent while, for a five-year fix it stands at 5.1 per cent, according to Moneyfacts.

How will the interest rate hold affect renters?

Renters are not immediately affected. Some landlords may decide to increase rents by smaller amounts if their mortgage increases whilst others will be fixed or own their property outright.

Rents are set by a variety of factors, including supply and demand, and so the hold is likely to have a minimal effect.

What will happen to savings rates?

Easy access savings rates can change at any point although they tend to move depending on interest rate rises and falls.

However if you have a fixed-rate account, the interest rate is set for the period of time the account is fixed for, so it will be unaffected by the news from the Bank of England.

If you are locking in a new account, it may be worth doing so sooner rather than later, as you can still obtain rates that easily beat inflation.

Myron Jobson, senior personal finance analyst at interactive investor, said: “Savings rates have seen little movement in recent weeks, although the overall trend has been downward. Shopping around for the best savings deals before they disappear remains a wise strategy.

“Those who can afford to lock away their money for five years or more should consider investing, as this offers the potential for long-term, inflation-beating returns that significantly exceed current savings rates.”

The best easy access savings rate on the market at the moment is Trading212’s cash ISA with a rate of 4.86 per cent.

The best one year fixed rate is with Cynergy Bank with a rate of 4.5 per cent.