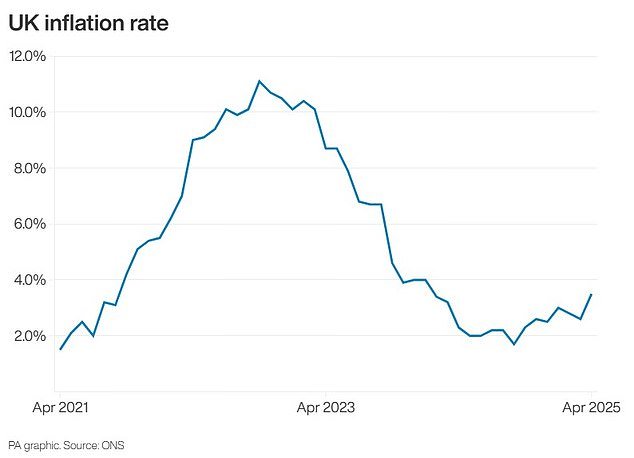

With UK inflation surging to its highest level for more than a year last month, many households will be concerned about the cost of living soaring once again.

The Office for National Statistics said Consumer Prices Index inflation hit 3.5 per cent in April, up from 2.6 per cent in March and the highest since January 2024.

The steep rise in inflation was also the largest since October 2022, at the height of the energy crisis – and comes after economists were expecting an increase to 3.3 per cent.

It comes after Ofgem’s energy price cap rose by 6.4 per cent last month, having fallen a year earlier. That arrived alongside a raft of bill rises for under-pressure households in ‘Awful April’ including hikes for water, council tax, mobile and broadband tariffs.

Economists believe the Bank of England may now tread more cautiously with cuts to interest rates after this month’s reduction from 4.5 per cent to 4.25 per cent.

Today, a series of financial experts have given MailOnline and This is Money their top tips on what consumers can do to protect their money during this period of higher inflation:

Review your budget

If you’ve had a pay rise in recent months you may have seen much of this swallowed up by the large increases in household bills and frozen income tax thresholds.

Experts say domestic energy bills are expected to fall this summer, but this may not be enough for struggling households battling with other rising utility costs.

Alice Haine, personal finance analyst at Bestinvest by Evelyn Partners, said: ‘For those still struggling with everyday bills, reviewing budgets to ensure expenditure comes in lower than household income is the simplest strategy, though that can be hard to achieve in reality.’

There are various free online tools available to help with putting together a budget, such as the one from Christians Against Poverty, which also runs money courses.

This is Money’s household budget calculator can help you work out the numbers – and our guide to budgeting can help you get a grip of your finances.

Budgeting can help with saving for the future, dealing with unexpected costs and taking control of debt or avoiding it altogether.

Consumers could also consider pausing big-ticket purchases and waiting until sale periods if they do not urgently need to buy a certain item.

Scott Gallacher, director at independent financial advisory firm Rowley Turton, said: ‘Keeping a tight grip on your costs is essential, whether you’re a household or a business.’

He urged consumers to ‘review spending, cut unnecessary expenses and don’t let rising prices creep into your lifestyle unchecked’.

Prime Minister Sir Keir Starmer and Chancellor Rachel Reeves at a Lidl in London yesterday

Check your subscriptions

Carrying out an audit of subscriptions and direct debits is an important part of budgeting to cut any wasteful expenditure.

You may find you have monthly outgoings to a service you do not even use anymore, and could find a cheaper deal from an equivalent provider.

TV subscriptions is a common area where people can find they are paying over the odds, having signed up on a cheap introductory deal then forgetting to cancel.

Kevin Mountford, co-founder of savings marketplace Raisin UK, said: ‘Clearly a lot will have been learned through the cost-of-living crisis, but it remains imperative that UK consumers look to budget effectively and cut out unnecessary spending by continuing to shop wisely.

‘For consumers, reviewing outgoings such as insurances, mobile and TV deals and switching to alternative products and providers or cancelling unused subscriptions altogether, can result in significant savings.’

If you are thinking about getting rid of a subscription but still want to keep the goods or services offered, you could also try calling the company and see if they can reduce the price to a more affordable level.

Mr Mountford added: ‘If you are looking to switch, do take into account the costs that can be associated with this to make sure it is worthwhile for you.

‘Taking the time to find the best deals not only helps make your money work harder but also keeps your return ahead of inflation.’

Get the best savings rate possible

News of the rise in the inflation rate for April is expected to slow the disappearance of top interest rates on savings accounts, which is good news for savers.

However, a higher inflation rate will also eat into savers’ returns – so it is important to make sure your money is working as hard as possible in an account.

Ms Haine said: ‘The very best savings deals are continuing to deliver a real return for now, once inflation is factored in, but the combination of higher prices and easing savings rates may dull the outlook from here.

‘With savings rates likely to ease back in the months ahead, securing a top deal now will lengthen the amount of time a saver receives an inflation-beating return.’

The best easy-access cash Isa savings accounts on the market are still offering close to 5 per cent, while fixed-term accounts can pay as much as 4.4 per cent.

Mr Gallacher added: ‘For savers and investors, the average savings account alone rarely keeps up with inflation over the long term. So ensure that you shop around for the best savings rates.’

Mark Hicks, head of active savings at Hargreaves Lansdown, said now was a good time to shop around for the best possible deals – and savers should consider shifting into a fixed deal.

He added: ‘It’s impressive how organisations are still competing for business, but we have seen savings rates start to ease off a little, so there are no guarantees of how long these great rates will be around.

‘It means anyone who opted for an easy access account for cash they won’t need for the next year or so might consider shifting into a fixed rate deal while rates are still so strong.’

> Check the best savings rates in This is Money’s independent tables

Workers shield from the rain as they cross London Bridge during the morning rush hour today

Use your Isa allowance

Every UK adult gets a £20,000 allowance each year to put money away tax-free in savings through a cash Isa, or in investments through a stocks and shares Isa.

This is growing in importance given the tax-free Personal Savings Allowance (PSA) has stayed at the same levels since its creation in 2016.

This allowance means you can earn interest without paying savings tax, but the benefit has been eroded away by inflation and frozen tax thresholds dragging more into higher rate and additional rate tax.

The allowance is £1,000 for basic-rate (20 per cent) taxpayers; £500 for higher-rate (40 per cent) taxpayers; and £0 for additional-rate (45 per cent) taxpayers.

If you are a couple with a joint account, the interest earned is split down the middle.

However, having an Isa can be a far better tactic because it means you can earn interest without having to be concerned about any tax impact, with up to £20,000 a year that can be contributed.

Ms Haine: ‘A tax-efficient savings strategy, such as taking advantage of your tax-free Isa allowance or topping up a pension is key.

‘While Isa reforms are still in contention, the Chancellor has confirmed that the £20,000 allowance will remain in place, which is why taking advantage of this ‘use it or lose it’ tax wrapper is a must for those that want to protect their savings from tax.’

The Chancellor is considering lowering the cash element of the annual Isa allowance, with rumours suggesting it could fall to £4,000 from £20,000, to encourage more people to put their money into investments.

But yesterday, Rachel Reeves confirmed on BBC Newscast that she does not plan to reduce the £20,000 overall limit on the amount that can be put into Isas each year but she will not confirm that the cash Isa limit won’t be cut.

> Read our essential guide to Isas and tax-free saving

Shift credit card debt onto a 0% balance transfer card

If you’re paying credit card interest, experts recommend that you shift the debt onto a 0 per cent balance transfer card.

This will pay off the debt on an existing card or multiple cars for you, so you then owe the card provider instead – but it will be interest-free for a fixed time.

This means your repayments can start to clear the debt, rather than paying the ever-growing interest on it.

David Stirling, director at Mint Mortgages and Protection, said: ‘For consumers the best tip is to try and pay down high interest debts, such as credit cards.

‘Inflation usually increases the interest rates charged on these debts.’

Eligibility calculators are available that can show acceptance chances for top cards without affecting creditworthiness.

Anyone getting such a card is warned to never miss the minimum monthly repayment, and clear the card before the 0 per cent period ends.

Economists believe the Bank of England may tread more cautiously with cuts to interest rates

Shop around for cheaper utility bills

The rise in inflation comes amid a raft of bill rises for households, including the biggest increase to water bills since at least February 1988, according to the Office for National Statistics.

Separate data from Compare The Market revealed average annual household bills increased to £5,606 in April this year – up from £5,494 in April 2024

Energy, council tax, and water bills rose by a combined average of £391, although the cost of car insurance has fallen by £268 on average year-on-year.

The rises last month during ‘awful April’ have increased the importance of shopping around for the best deal possible.

While this might not be possible with water supply, there is plenty of choice in the market when it comes to energy, broadband and mobile phone contracts.

Guy Anker, cost of living expert at Compare the Market, said: ‘With the average bill increasing again this year, it’s more important than ever for households to shop around for cheaper deals on bills where they can.

‘You could save a significant amount of money by checking a price comparison site for deals on your regular outgoings, such as car and home insurance, energy bills, broadband, and credit cards, when they’re up for renewal.’

| Household bill | April 2024 cost | April 2025 cost | Change (£) |

|---|---|---|---|

| Energy | £1,690 | £1,849 | +£159 |

| Home insurance | £223 | £212 | -£11 |

| Motor insurance | £930 | £662 | -£268 |

| Water | £480 | £603 | +£123 |

| Council tax (Band D) | £2,171 | £2,280 | +£109 |

| Total cost | £5,494 | £5,606 | +£112 |

| Source: Compare The Market | |||

Think about your cash – do you have too much?

Financial experts say it is important to ensure you have enough cash available for emergencies but also note that the real value of this will fall as inflation rises.

Rob Mansfield, independent financial advisor at Rootes Wealth Management, said: ‘Be deliberate with your cash. We all need an emergency fund for when the heating packs up or your car breaks down.

‘But holding too much cash leaves you exposed to inflation. While you might be gaining interest in cash, if inflation is higher, the real value of your money may fall. For genuine longer term savings, investments may be the answer.’

People are recommended to have an emergency savings fund in readily accessible cash of three to six months’ post-tax earnings or essential expenditure. Above this, they could consider investing for better long-term returns.

Riz Malik, director at R3 Wealth, added: ‘To beat inflation, your savings must work harder than rising prices. Don’t treat your money as one lump sum, split it by timeframes and invest accordingly.

‘While many are taking advantage of higher cash rates, other options may offer more benefits, especially for higher-income taxpayers. If in doubt, an independent financial adviser can help you find the right mix.’

Other experts advise looking into stocks and shares for those who are trying to get a better return – although this is a far higher-risk strategy that could result in you losing some or all of your money.

Faisal Sheikh, managing director at Monmouth Capital, said: ‘For private investors with long term savings, if you want to beat inflation, get out of cash and into equities.’

Meanwhile David Belle, founder and trader at Fink Money, recommended large market capitalisation US stocks such as Meta, Nvidia, Apple and Google.

But Ross Lacey, independent financial adviser at Fairview Financial Management, warned: ‘Any investment strategy needs to be implemented within the context of a wider financial plan.’

Get a mortgage rate locked in

Data from Moneyfacts shows the average two-year fixed mortgage deal is now 5.11 per cent – compared to a month ago when it was 5.23 per cent and a month earlier when it was 5.33 per cent.

The market has even seen some deals with rates of less than 4 per cent in recent months after a mini-price war broke out between mortgage providers.

Justin Moy, managing director at EHF Mortgages, said some mortgage lenders allow people to reserve a mortgage deal before they have found their ideal property.

He pointed out that this helps with ‘avoiding rate increases that may happen with little to no notice, but if rates fall borrowers can jump on that saving too’.

While future changes to mortgage rates are uncertain, experts suggest the Bank of England is not expected to react to the rise in inflation – which it had forecast – and therefore borrowers can expect lower mortgage rates to stick around.

Sarah Coles, head of personal finance at Hargreaves Lansdown, said the lower rates are ‘music to the ears of anyone with a remortgage around the corner’.

But she added: ‘There’s enough uncertainty around at the moment for it to be tricky to guarantee the future path of mortgages. If you have a remortgage coming up, it’s well worth securing a rate now, and then looking again when your deal is up.

‘If rates have fallen again, you can shop around for something better, and if the market has been caught by surprise, you’ll have locked in a decent deal.’

> Mortgage finder: Check the best rate you could apply for

Should you invest in government bonds?

Another option recommended by some experts is investing in UK Government bonds, known as gilts. These see you lend money to the Government in return for regular interest and your money back at the end of the term.

Last week, a 30-year gilt paying 5.375 per cent interest until January 2056 was launched by the UK government. Investors can sell out before then but should be aware that the price of the bond on the second hand market could move up or down over its lifetime.

Gabriel McKeown, head of macroeconomics at The Sad Rabbit newsletter, said: ‘Despite the recent rate cut from the Bank of England, we are still in a high-yield environment whereby savers and investors are able to lock-in inflation-beating annual returns via government bonds.’

He went on: ‘Furthermore, the wider credit market is currently a favourable source of returns that exceed inflation, while remaining risk-adjusted.

‘Diversified investment grade credit funds allow investors to spread their risk among hundreds of the largest companies, receiving a quarterly interest payment, with a far lower risk exposure given the number of companies within the fund.

‘Currently many of these funds are beating inflation, and can form a great portfolio constituent for the long-term.’

Mr McKeown said these can be used alongside other savings products, such as money market funds and traditional savings accounts, to ensure your money is not eroded by inflation – and also avoiding the risk posed by equity markets.

Kundan Bhaduri, entrepreneur at The Kushman Group, pointed to NS&I index-linked bonds as the ‘smarter move for consumers’, if they are worried about inflation returning.

However, this NS&I product is only available to customers who purchased the original certificates and decide to keep them at each maturity length. It has not been on sale since 2010.

Mr Bhaduri also said investing in the stock market also offers the opportunity to get a rising income return.

He added: ‘FTSE 100 dividend stocks currently yield 3.9 per cent with growth potential, and for cautious savers, inflation-linked gilts provide sovereign protection without stock market volatility.’

SAVE MONEY, MAKE MONEY

Isa offer

Isa offer

40% off account fees for six months

Fix energy bills

Fix energy bills

Check price cap beating deals with uSwitch

Fee-free Isa investing

Fee-free Isa investing

Free share and ETF dealing, no account fee

5.70% cash Isa

5.70% cash Isa

Rate boosted for three months, then 4.85%

Get £20 off an MOT

Get £20 off an MOT

£20 This is Money Motoring Club voucher

Affiliate links: If you take out a product This is Money may earn a commission. These deals are chosen by our editorial team, as we think they are worth highlighting. This does not affect our editorial independence. Terms and conditions apply on all offers.