[ad_1]

Index funds track the performance of a benchmark index, such as the S&P 500, by investing in the index portfolio. Since these passively managed funds require less research and trading activity than actively managed funds, they typically charge much lower fees. This low-cost approach has given households access to well-diversified, efficient portfolios that generate higher retirement savings.

Index funds are commonly organized as either mutual funds or exchange-traded funds (ETFs), and organizational differences lead to distinct investor tax treatment. Although mutual funds and ETFs can hold identical portfolios of securities, investors can face very different tax outcomes. In mutual funds, investors may owe taxes on capital gains because of other investors’ actions, even if they did not sell any shares themselves. This periodic taxation can reduce long-term after-tax returns. In contrast, investors in ETFs typically pay capital gains taxes only when they sell their shares, giving them greater control over their tax liabilities and often resulting in higher after-tax returns. Should an investor pass away without selling their ETF, the step-up in basis erases the accumulated tax liability.

This paper argues that these differences reflect a flaw in the taxation of certain pooled investment vehicles. The current tax treatment violates basic principles of horizontal tax equity by disadvantaging mutual fund investors relative to otherwise identical ETF investors. A range of policy options could equalize the tax treatment of mutual funds and ETFs, though they differ in how they affect investor outcomes, market efficiency, and tax revenues. This paper evaluates these options through the lens of equity, efficiency, and administrability to highlight the tradeoffs involved in reforming index fund taxation.

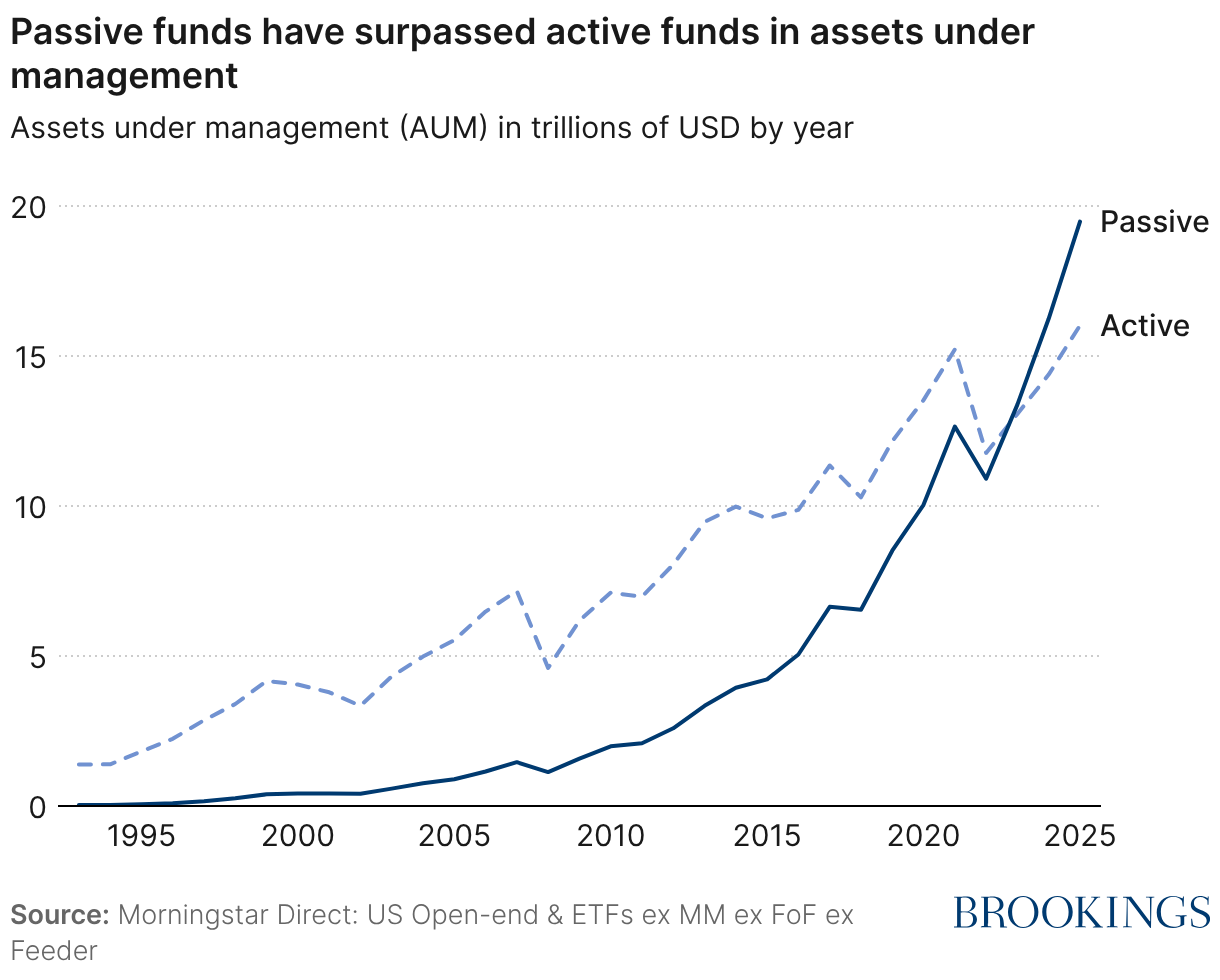

Rather than managing their own portfolios directly, households often invest through pooled investment vehicles that aggregate and deploy the capital of many shareholders. Index funds—whether structured as mutual funds or ETFs—represent a particularly important type of pooled investment vehicle. By passively tracking a market index, such as the S&P 500, index funds offer broad diversification at low cost. Since the launch of the first index funds in the 1970s, the rise of passive investing has transformed capital markets: passive funds recently surpassed active funds in total assets under management (see Figure 1).

This growth has been prompted by academic research that advocates holding a broad market portfolio, and has been further reinforced by the cost-effectiveness of passive funds: in 2022, for example, the asset-weighted average fee of active funds was 0.59%, compared to just 0.12% for passive funds.

Figure 1

But while both ETFs and mutual funds can be used to create passive index portfolios, they are taxed differently. As a result, investors may experience large differences in after-tax performance. One of the primary reasons for this is the difference in how mutual funds and ETFs satisfy investor redemptions.

Mutual fund taxation

When an investor withdraws money from a mutual fund, the fund manager typically sells some of the underlying assets to generate cash to give to the investor. But if the fund’s assets have increased in value since the fund manager first purchased them, then this sale triggers a capital gains tax for all non-redeeming investors in the fund at year’s end. In other words, in a mutual fund, a withdrawal by one investor can trigger capital gains taxes for all investors.

ETF taxation

In contrast, ETFs are structured differently. If an investor exits an ETF position, there are two possibilities. First, the investor can sell the ETF shares to another investor in the secondary market. In this case, because the shares simply change hands, the fund does not need to sell any underlying assets, so no fund-level capital gains taxes are triggered. Second, ETF shares may be redeemed by specialized market participants known as “Authorized Participants.” These Authorized Participants play a central role in providing liquidity and keeping ETF share prices aligned with the value of their underlying assets. Authorized Participants (APs) buy the ETF shares from the investor in the secondary market (the stock exchange where ETF shares trade) and deliver them to the fund through the primary market (where ETF shares are created or redeemed directly with the fund) in exchange for a basket of the underlying securities from the fund portfolio. These transactions are known as “in-kind” transfers and are not a taxable event under §852(b)(6) of the tax code.

It is important to note that both ETF investors and mutual fund investors pay taxes on capital gains when they sell their fund shares. The key difference is that ETF investors incur capital gains taxes effectively only when they sell shares, while mutual fund investors may also incur taxes while continuing to hold their position. In this sense, ETF investors are not avoiding taxes, but rather, they are deferring them until they choose to exit the position.

Implications

As a consequence of these different tax structures, investors in mutual funds and ETFs may earn different returns even if the mutual fund and ETF hold the exact same underlying assets.

Regulatory responses

In recent years, there have been several different regulatory proposals designed to address these tax differences. In 2021, Senator Wyden introduced a proposal to eliminate the in-kind redemption exemption under Section 852(b)(6), effectively bringing ETF tax treatment in line with that of mutual funds. More recently, the bipartisan GROWTH Act has proposed moving in the opposite direction by reforming tax policy to defer the realization of all capital gains until the point that an investor (not the fund manager) sells the assets, effectively bringing mutual fund tax treatment in line with that of ETFs.1 Both proposals would eliminate the disparity between ETFs and mutual funds, but they would have very different implications for investors and efficiency. In what follows, we discuss the details.

Trends in household ownership of mutual funds and ETFs

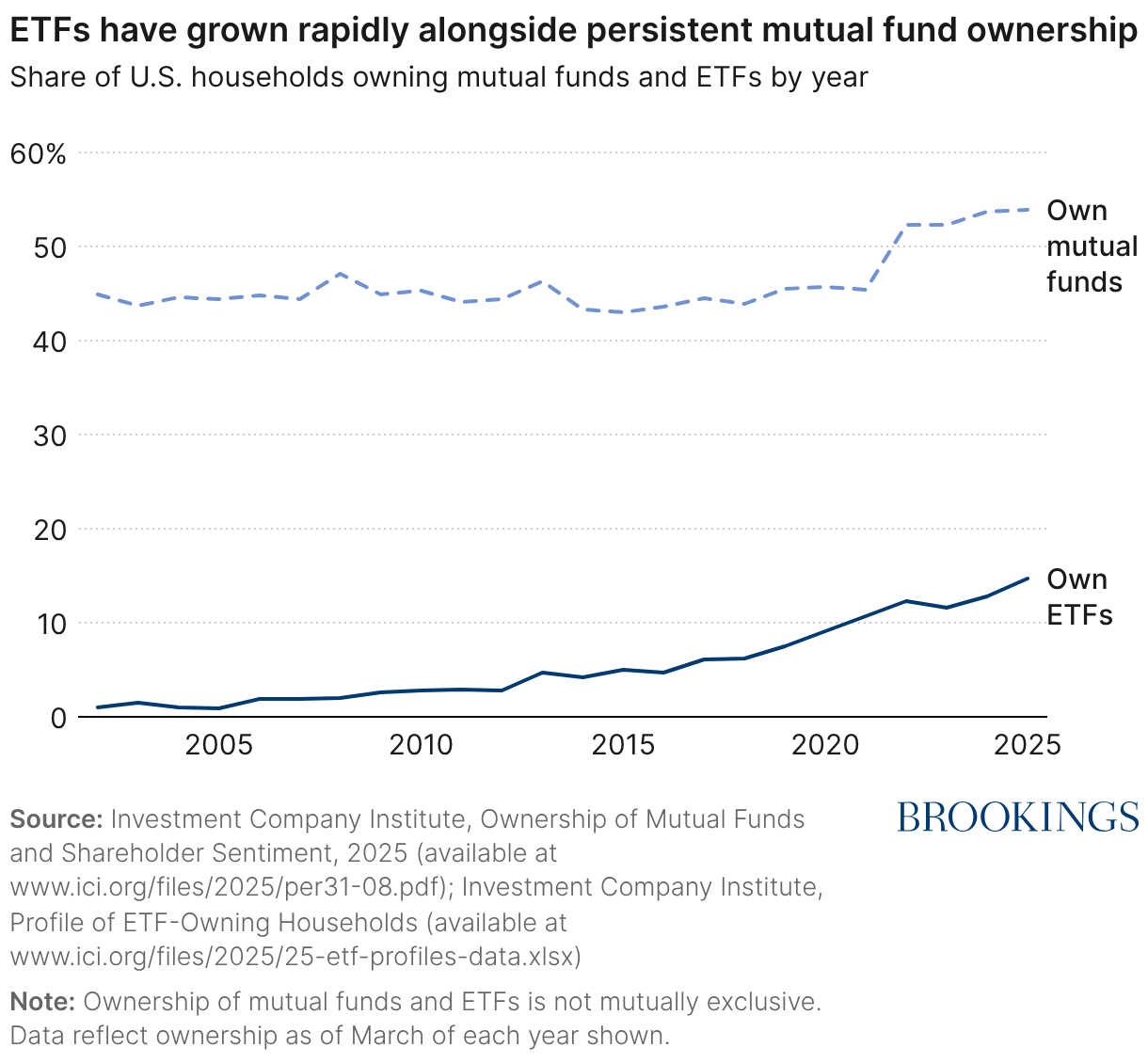

The tax differences between mutual funds and ETFs would be of limited policy importance if only a small or non-representative group of investors were affected. In reality, both vehicles are widely held by U.S. households. Understanding who owns each type of fund—and how those funds are used—is essential for evaluating the implications of their differential tax treatment. This section documents three patterns: the rapid growth of ETFs alongside persistent mutual fund ownership, the concentration of ETF ownership among higher-income households, and differences in how investors use these vehicles in their financial planning.

Growth and scale of ownership

Households have long relied on mutual funds as a primary vehicle for well-diversified investing, particularly for retirement savings. ETF ownership, by contrast, has expanded rapidly over the last two decades. Using data from the Investment Company Institute (ICI), Figure 2 shows that while mutual fund ownership has remained stable—generally between 30 and 45% of households have owned mutual funds over the past 25 years—ETF ownership has grown from negligible levels in the early 2000s to nearly 15% of households by 2025.

Figure 2

This growth means that ETFs are no longer a niche product. Millions of households now hold ETFs, and many hold them alongside mutual funds. At the same time, mutual funds remain one of the most widely used investment vehicles in the United States. The coexistence of the two structures—often holding similar underlying portfolios—makes differences in their tax treatment economically meaningful. As ETF ownership continues to expand, any systematic tax advantage associated with one structure rather than the other makes differences in their tax treatment meaningful.

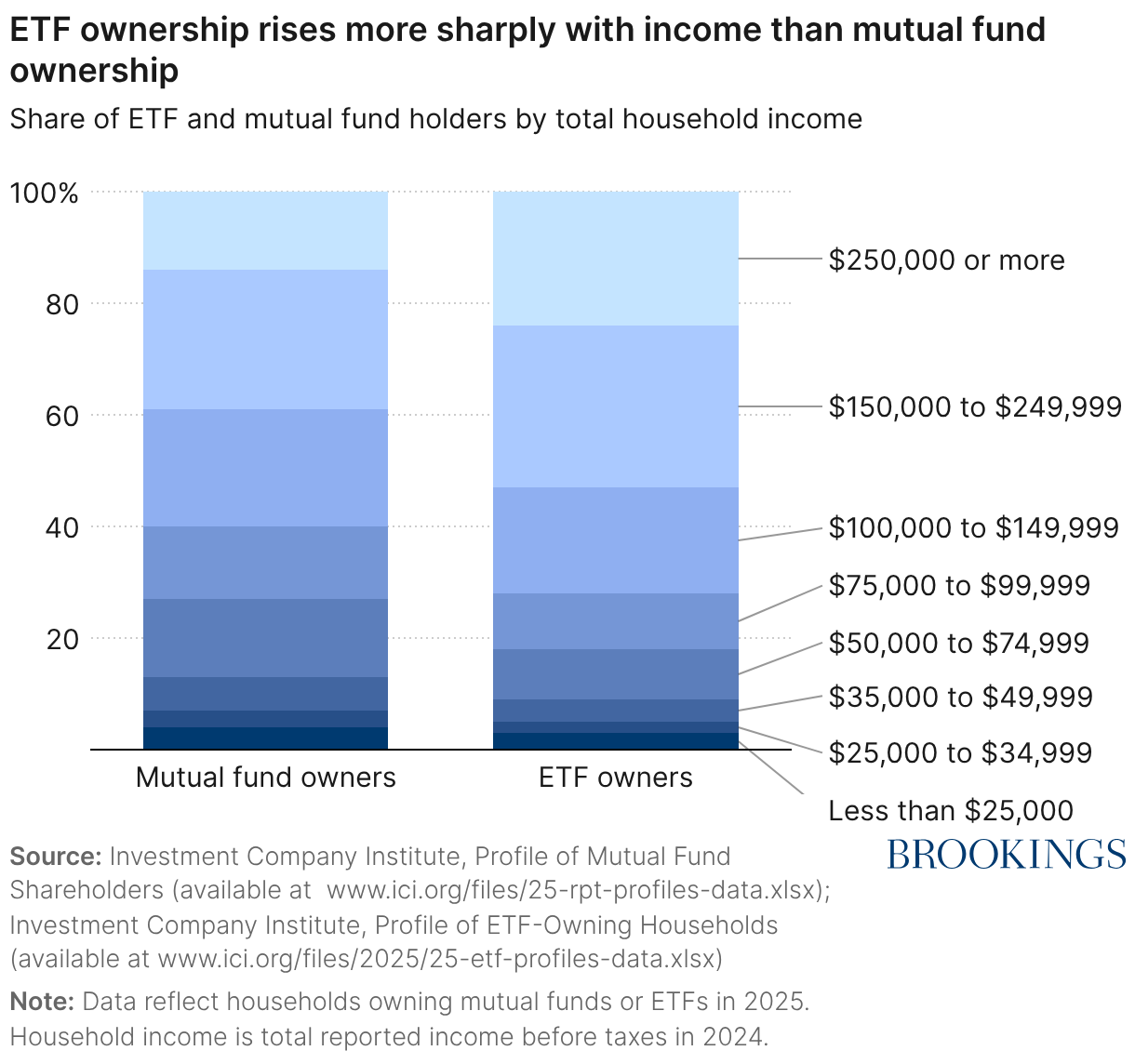

Ownership by income

Mutual fund and ETF ownership also differ systematically by income group. Figure 3 reports ownership rates by household income. ETF ownership rises sharply with income: higher income households are more likely to report holding ETFs than lower-income households. Mutual fund ownership, while also positively correlated with income, is more evenly distributed across the income distribution.2

Figure 3

These patterns matter for tax policy. The ability to defer capital gains is particularly valuable for investors with larger taxable portfolios and longer investment horizons. Higher-income households are also more likely to have access to financial planners, and to actively manage the tax consequences of their investment decisions. As a result, the current tax structure—under which ETF investors can generally defer fund-level capital gains realizations while mutual fund investors may incur taxes triggered by other shareholders’ redemptions—tends to deliver larger benefits to households at the top of the income distribution.

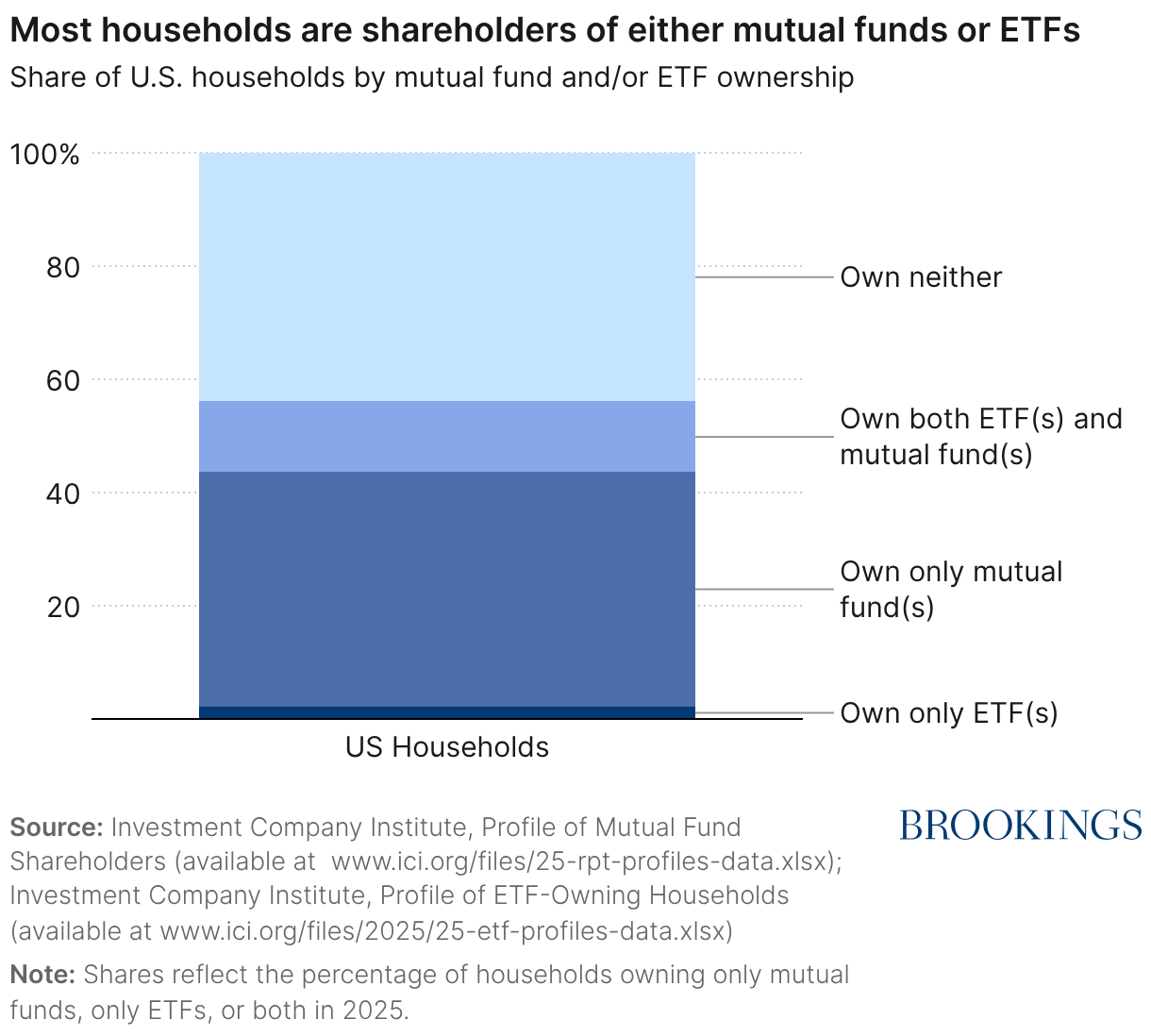

At the same time, many households continue to rely primarily on mutual funds, and a meaningful share holds only mutual funds rather than ETFs (Figure 4). The distributional asymmetry is therefore not trivial: the tax differences between fund structures do not affect all households equally, and the advantages of deferral are concentrated among higher-income households.

Figure 4

Investment purposes and financial goals

Beyond differences in income, mutual fund and ETF investors also report somewhat different financial objectives. Figure 5 summarizes households’ primary financial goals. Retirement savings is the dominant purpose for both mutual fund and ETF investors, underscoring the central role these vehicles play in long-term wealth accumulation. However, ETF investors are relatively more likely to cite tax reduction or shorter-term financial goals than mutual fund holders.

Figure 5

This distinction reinforces the relevance of tax timing. For households using funds primarily as long-term retirement vehicles, unexpected capital gains distributions can reduce after-tax returns and disrupt planning, particularly when taxes are triggered by the actions of other investors. For households that are more tax-sensitive or actively managing taxable portfolios, the ability to defer realization until sale provides greater control over the timing of tax liabilities. In this way, differences in fund structure interact with differences in investor objectives.

A large share of mutual fund and ETF assets are held in tax-preferred retirement accounts, such as 401(k)s and IRAs, where capital gains distributions do not trigger immediate tax liability. In those settings, differences in fund-level realization are less meaningful. However, taxable accounts still represent a significant portion of household financial wealth. The structural differences described in this paper, therefore, matter for any investor holding funds outside of tax-deferred accounts. Importantly, the fact that some assets are shielded from current taxation does not eliminate the asymmetry in how otherwise identical investments are treated in taxable accounts.

Implications for distribution and investor outcomes

Taken together, these patterns show that differences between mutual fund and ETF holders are neither minor nor abstract. ETFs are widely held and growing rapidly, yet their ownership is more concentrated among higher-income households who are best-positioned to benefit from capital gains deferral. Mutual funds remain a core retirement savings vehicle for a broad group of households, including many who do not actively manage the tax consequences of their investments.

As a result, differences in fund structures do more than alter the timing of tax payments. They shape after-tax wealth accumulation across households and may amplify disparities in long-term investment outcomes. These distributional patterns underscore the importance of evaluating whether current law treats economically similar investments consistently and whether the tax system aligns liabilities with investors’ own decisions rather than the actions of other shareholders.

A framework for evaluating index fund taxation

To assess whether current law achieves its objectives, it is useful to anchor the discussion that follows in a set of widely accepted tax policy principles. First, a well-designed tax system should treat economically similar investors similarly, so that tax outcomes associated with the same income do not depend on the particular vehicle through which an investment is held. Second, tax rules should interfere as little as possible with investment decisions. Investors should choose portfolios based on risk and return, rather than tax consequences based on other investors’ actions. Likewise, fund managers should manage portfolios based on investment fundamentals, not on incentives created by tax-driven mechanisms. Third, the tax system should be transparent and administrable, so that investors and administrators can reasonably determine when and why taxes are owed.

The sections that follow describe the regulation and tax treatment of mutual funds and ETFs in more detail and use these principles to clarify where current rules align with—and depart from—core objectives of equity, efficiency, and simplicity.

Regulation of mutual funds and ETFs

Both mutual funds and ETFs are typically structured as a special type of corporation called a Regulated Investment Company (RIC). This designation allows them to avoid paying the corporate income tax as long as they meet certain requirements outlined in the Internal Revenue Code under Subchapter M, the most important being that a fund must distribute at least 90% of its taxable income to investors each year.3 The distributed income is then taxed at the investor level. This tax treatment is similar to the tax treatment of other pass-through business forms.

Mutual funds and ETFs also expand and contract with investor demand. When investors put more money in, the fund issues new shares; when investors want their money back, the fund redeems shares. Shares must be issued and redeemed at the value of the underlying portfolio—known as the net asset value (NAV).4 How a manager meets these requirements—specifically, how they create and redeem shares—can lead to substantial implications for investors’ tax liabilities.

As discussed above, mutual funds and ETFs differ in how they handle investor transactions. Specifically:

- Mutual funds: Investors buy or sell shares directly from the asset manager. Orders are reconciled once per day, typically after the close of the trading day, with the transaction price determined by the fund’s same-day NAV.

- ETFs: Investors can buy or sell shares throughout the day on the secondary market, transacting directly with other buyers and sellers, just as they would with any exchange-listed security. The trading price is determined by supply and demand and, therefore, fluctuates throughout the trading day. Their counterparty might be another investor or a market maker, but it could also be a specialized trader called an Authorized Participant (AP). APs are the only parties who may transact directly with the asset manager to create or redeem ETF shares.

A key distinction between these two types of funds is how they keep their share price aligned with the fund’s NAV. Mutual funds trade only once each day, at the close of the trading day. Creations and redemptions are priced at the NAV, ensuring a match between the fund’s price and the value of the assets it holds.

ETFs, by contrast, typically rely on a specialized process called in-kind creation and redemption to incentivize APs to generate supply or demand. ETF creations and redemptions occur in the primary market between the ETF and a small group of designated traders known as Authorized Participants (APs). APs are typically large financial institutions selected by the asset manager before the fund’s launch.

This process works through a natural arbitrage mechanism:

- If the ETF’s market price rises above its NAV, APs have an incentive to create new shares by delivering a bundle (basket) of the fund’s underlying securities to the fund in exchange for new ETF shares, which can then be sold for a profit.

- If the ETF’s market price falls below its NAV, APs redeem (sell back) shares by selling them back to the fund in exchange for the underlying securities, which can be profitably sold for more than the ETF’s market price.

This creation/redemption process keeps the ETF’s intra-day price closely tied to its NAV, as required by the Investment Company Act of 1940, while also ensuring liquidity in the secondary market.

While mutual funds are also permitted to use in-kind redemptions, they do so infrequently, typically only in response to unusually large redemption requests or periods of market stress.5

Taxation of regulated investment companies (RICs)

As previously mentioned, RICs avoid the corporate income tax if they distribute at least 90% of their income to shareholders each year. This structure spares investors from the “double taxation” that applies to traditional C-corporations. For example, if a C-Corporation earns $100, it first pays the 21% corporate income tax ($21), leaving $79 in post-tax income. Any portion of that amount that is distributed to shareholders is then taxed again at the individual level. By contrast, a RIC pays no corporate tax on its income; instead, its income passes directly to investors and is taxed only once, at the individual level. The key difference between mutual funds and ETFs concerns when this tax is paid by the investor.6

RICs can earn income from a few different sources:

- Interest and dividend income – A portfolio holding dividend-bearing stocks will generate dividend income while one holding bonds will earn interest income; in both cases, this income must be distributed to investors in the year it is earned.

- Capital gains – A portfolio that sells a stock or other security for a taxable capital gain will generate capital gains income that must be distributed to investors in the year it is earned.

RIC investors can incur a tax in two ways:

- All investors are taxed on income that is distributed by the fund in the year the distribution occurs. In mutual funds, capital gains distributions can arise when the fund sells appreciated assets to meet redemptions, even if the shareholders did not personally sell any shares. In ETFs, the in-kind creation/redemption process can allow portfolio managers to rebalance without triggering a capital gain.

- Investors of both mutual funds and ETFs will incur capital gains taxes if they sell their fund shares for more than the original purchase price.

This two-layered tax—arising from both fund-level actions and investor-level sales—means that shareholders can face tax bills for gains they did not choose to realize and income they did not actually receive. As the next section explains, this burden falls especially hard on mutual fund investors.

How fund structure shapes investor tax outcomes: creation and redemption

Although mutual funds and ETFs often hold similar assets, they differ sharply in how investor purchases and redemptions are processed and this difference drives markedly different tax outcomes.

Mutual funds

Mutual funds generally meet investor redemptions in cash. To raise that cash, fund managers may need to sell assets. For example, when an investor redeems $100,000 of mutual fund shares, the fund’s manager may need to sell $100,000 of underlying assets to generate the necessary cash to give to the departing investor. If those assets have appreciated, the sale realizes capital gains that are passed through to all remaining shareholders.

This creates a tax externality: investors who remain in the fund bear tax consequences generated by others’ redemption decisions. While mutual funds typically hold some cash to meet routine outflows, large or sustained redemptions eventually force asset sales. When appreciated assets are sold, long-term investors incur tax liabilities. In other words, they are effectively forced to subsidize the exit of other shareholders.7

Moreover, new investors may also face a tax overhang: if a fund has a pool of unrealized gains, it can generate a tax liability for new investors even though the gains accrued before they invested in the fund. To see this, consider a simple example. Suppose a mutual fund holds $100 million in assets, of which $80 million represent unrealized gains. Imagine a new investor buys shares in the fund on Monday. On Tuesday, a different investor redeems a large position, forcing the fund to sell assets to cover the redemption, resulting in a realization of $8 million in capital gains. This $8 million gain must be distributed pro-rata, or in proportion to relative ownership shares, to all remaining shareholders—including the new investor. Thus, the new investor faces a tax liability on gains that accrued before they joined the fund.

Finally, mutual fund managers also regularly distribute capital gains to their investors at the end of the year.8 Distributed gains cause a drag on the investor’s after-tax performance, since money paid out in taxes does not continue to earn compound returns in the fund.

In sum: because mutual fund shareholders have no control over when the fund realizes capital gains, they face uncertainty about their annual tax bill and reduced after-tax performance.

ETFs

ETFs, by contrast, tend to meet redemptions through in-kind transactions. Instead of selling securities to raise cash, the fund transfers a basket of its underlying holdings to an Authorized Participant in exchange for the ETF shares being redeemed. Because the redemption is conducted in-kind rather than through a cash sale, Section 852(b)(6) of the tax code provides that the fund does not recognize capital gains or distribute them to shareholders. In this way, shareholders avoid fund-level capital gains distributions that would otherwise result from selling those same securities for cash.

If an ETF needs to rebalance, the portfolio manager can use this in-kind creation/redemption process to remove assets that have appreciated in value without triggering a taxable event. This process relies on authorized participants (APs), who are incentivized to trade because they can profit from arbitraging differences between the ETF’s market price and the net asset value (NAV) of its underlying portfolio. For example, when the ETF trades at a premium to NAV, an AP can buy the underlying securities, deliver them to the ETF in exchange for newly created ETF shares, and then sell those shares at the higher market price, earning an arbitrage profit9.

Most importantly, both mutual fund and ETF investors will pay taxes when they exit their position in the fund. The key difference is when they pay taxes: ETF investors will defer paying the tax until they withdraw from the fund, while mutual fund investors may have to pay the tax before they withdraw from the fund due to the tax externality and annual capital gains distributions. Importantly, this difference is material: it can dramatically change the wealth accumulated by investors in the long-run. Recent estimates suggest that this tax efficiency has increased the long-term after-tax return of ETF investors by 1.05% per year, relative to mutual fund investors (Moussawi, Shen, and Velthuis 2025).

Example

Figure 6 shows a detailed numerical example of the difference in taxation for mutual fund and ETF investors. 10 Imagine there are two funds that are identical in every way — each indexed to follow the market and holding the exact same portfolio of assets — except one is organized as a mutual fund and the other as an ETF. For convenience, assume they both start with a net asset value (NAV) of $10 per share.

Figure 6

After the first year, the market increases 10% so both funds increase to $11 per share. But at the end of the year, the mutual fund must distribute this capital gain to its investors, who are then taxed at the long-term capital gains rate of 15%. In contrast, the ETF does not distribute the capital gain, and this money remains in the portfolio, where it can continue to increase in value. As a result, at the start of the second year, the mutual fund has a NAV of $10 per share while the ETF has a NAV of $11 per share.

Now imagine that the market increases 10% again over the second year, but this time, both the mutual fund investor and the ETF investor decide to exit the fund at the end of the year. This triggers a capital gain for both of them, and they each pay a capital gains tax of 15%. Crucially, notice that the tax bill in the second year is larger for the ETF investor than for the mutual fund investor – this is because the ETF investor deferred all taxes until the end while the mutual fund investor paid year-by-year. In other words, both investors eventually pay taxes on all their capital gains, the only difference is when they pay the tax. But this timing turns out to be important.

Even though both funds held the same underlying portfolio of assets, the ETF investor ends up with a larger after-tax profit ($1.78) than the mutual fund investor ($1.70). Notice also that because the ETF investor earned more, they also pay more in total taxes ($0.32 vs. $0.30). But importantly, both investors paid exactly 15% of their profits in taxes – the ETF investor did not dodge any taxes, they simply deferred the taxes which allowed their money to grow to a larger balance in the fund.11

Tax deferral increases after-tax wealth even when tax rates and investments are the same

The distinction is clear. In a mutual fund, portfolio gains may be realized throughout the year when the fund sells appreciated assets, and those gains are typically distributed and taxed at year-end—even for investors who do not sell their shares. Thus, even though both the mutual fund and the ETF in this example are index funds holding the same portfolio of assets, investors achieve different after-tax outcomes. While the tax externality we describe is not unique to passive index funds,12 the risk is acute in index funds because most investors choose the fund explicitly because it is passive with low turnover (Poterba and Shoven (2002), Moussawi, Shen, Velthuis (2025)) making it especially costly if another investor sells and causes a taxable event for the remaining investors.

In sum, the example highlights three key points:

- Investors will tend to accumulate more wealth in ETFs than otherwise identical mutual funds. This is because deferring taxes allows their money to remain in the fund, and thus, this money continues to appreciate in value.

- Both mutual fund and ETF investors eventually pay the same proportion of their profits in taxes. In other words, ETF investors do not avoid taxes, they defer them until they choose to exit their position.

- Because ETF investors will tend to accumulate more wealth and they pay taxes only at the end, when they choose to exit their position, ETF investors will tend to pay a higher dollar amount in taxes.

In short, the structure of ETFs allows investors to earn higher wealth and generate more tax revenue. Figure 7, below, demonstrates the cumulative impact on a long-term investor. The figure plots the account balance of a hypothetical investor who invests $10,000 in an index mutual fund (gray dotted line) versus an index ETF (solid black line) over the period 2010 to 2025. The figure assumes both funds invest in the S&P 500, but the mutual fund distributes capital gains at the end of each year that are taxed at 15%, while the ETF does not.13 Over time, this generates a large disparity in outcomes and by 2025, the ETF account balance is almost 25% higher than the mutual fund balance ($61k vs. $49k).

Figure 7

Tax deferral and ETFs: Heartbeat trades

While it is clear that ETFs are tax advantaged in a manner that benefits investors, managers can also use in-kind redemptions strategically even when there are no significant investor withdrawals. 14 In these cases, the transactions are used not to meet investor redemptions, but to remove appreciated assets from the portfolio without triggering a taxable gain. This use of in-kind transactions for portfolio management has drawn increased scrutiny of the ETF structure and raised questions about the optimal taxation of index funds.

In practice, this mechanism allows ETFs to rebalance without realizing gains. An Authorized Participant (AP) first delivers a basket of securities to create new ETF shares, increasing the size of the fund, and then redeems shares for a different basket that contains the appreciated securities the fund seeks to shed. Because these exchanges occur in-kind, the ETF can remove appreciated assets from the portfolio without realizing capital gains. Such transactions are often referred to as “heartbeat” trades because the number of ETF shares outstanding briefly expands and then contracts, resembling a heartbeat on an electrocardiogram.15

One well-known example of this behavior is a heartbeat trade. A heartbeat trade refers to a back-to-back in-kind creation and redemption trade, often coordinated around portfolio rebalancing events, that washes away capital gains. For example, imagine an ETF that tracks the S&P 500 index. In 2024, the S&P 500 index removed American Airlines (ticker: AAL) and added Palantir Technologies (ticker: PLTR). As a result, the fund needs to exit its position in AAL (assume the position is worth $50 million) and instead buy $50 million worth of PLTR. Because AAL appreciated in value since the fund initially purchased it, selling it would trigger a capital gain and a resulting tax for investors. So instead, the fund uses a heartbeat trade.

To do this, an AP delivers a basket of $50 million in PLTR stock to the ETF and in return receives $50 million worth of newly created shares in the ETF.16 Thus, the trade increases the total size of the ETF by $50 million (since new assets entered and no assets left). Then, the next day, the AP sells $50 million worth of shares in the ETF back to the fund but instead of receiving their cash value they receive a basket of $50 million in AAL stock. The fund is now back to its original size. Finally, the AP then sells the AAL on the stock exchange to generate $50 million in cash. The net effect is that the fund no longer owns any AAL stock and instead owns PLTR stock, but because the redemption from the ETF was in-kind, the ETF was able to exit its position in AAL without realizing a capital gain. Thus, even though the transaction was motivated by portfolio management, not investor flows in and out of the fund, there is no taxable event.

A 2019 Bloomberg article identified more than 2,200 heartbeat trades worth over $300 billion between 2000 and 2019, with most of the trades occurring after 2013. This pattern suggests that heartbeat trades increased substantially in recent years, drawing growing scrutiny from policymakers and analysts (see Colon (2023)).

Example

While these transactions have drawn scrutiny, they are often misunderstood as eliminating capital gains when in fact they are altering the timing of realization. To clarify this distinction, Figure 8 presents a simple numerical example that traces an ETF investment over several years and compares outcomes with and without a heartbeat trade.

Figure 8

The example shows two cases that are identical except for how the fund rebalances an appreciated position at the start of Year 2. In the Baseline case, the fund sells the appreciated asset for cash in order to rebalance; in doing so, the fund realizes a capital gain that results in a capital gain distribution to investors. In the heartbeat case, the fund removes the appreciated asset through an in-kind transaction, avoiding fund-level realization. In both cases, the investor purchases ETF shares at the same initial price and sells at the end of the holding period.

In the Baseline scenario, the investor pays capital gains twice: first when the fund distributes realized gains to rebalance the portfolio, and again when the investor sells fund shares at exit. In the Heartbeat case, the rebalancing does not trigger a distribution, so the investor pays capital gains only when selling fund shares.

Importantly, Figure 8 shows that heartbeat trades do not eliminate capital gains taxation. In both the baseline scenario and the heartbeat scenario, investors eventually pay the same proportion (15%) of their profits in taxes. The key difference is that the heartbeat trade prevents capital gains from being realized at the fund level during portfolio rebalancing, thereby deferring the realization of taxes until the investor chooses to sell. As in Figure 6, this deferral allows the gains to remain invested in the fund for longer, increasing after-tax wealth without eliminating tax liabilities.

Other tax deferral strategies

Two other tax deferral strategies play important roles in the investment company market.

First, in 2001, Vanguard patented a unique fund structure that creates ETF share classes within a mutual fund. The ETF share class enables the fund to use in-kind redemptions to wash away capital gains for all shareholders, including investors in the mutual fund. It was widely reported that this structure allowed Vanguard to effectively eliminate all capital gains distributions across both share classes. Vanguard’s patent on this design expired in 2023, opening the door for competitors to adopt a similar approach. To date, more than 60 applications have been filed petitioning the SEC for approval to set up similar funds (Sizemore (2025)). The SEC has since begun approving the first ETF share class structures following the patent’s expiration.

Second, SEC Rule 6c-11, which was adopted in 2019, made it easier to set up an ETF and led to an increase in mutual funds converting to ETFs. As discussed in Moussawi, Shen, and Velthuis (2025), a mutual fund converting to an ETF is not a taxable event, and the new fund can then use in-kind redemptions to defer capital gains taxes for its investors. In 2024 alone, 55 mutual funds converted to ETFs (Lee (2024)).17

Policy options to address the negative externality

The divergence in tax treatment between mutual fund and ETF shareholders violates three widely accepted principles of good tax policy: equity, efficiency, and simplicity. As described above, two investors can invest in otherwise identical index funds but experience very different tax outcomes, raising concerns about horizontal inequity. In mutual funds, taxes can be triggered by other investors’ actions rather than an investor’s own decisions, creating a negative externality that reduces economic efficiency by distorting investment incentives and lowering after-tax returns. Moreover, the mechanisms used to avoid these distortions within the existing framework introduce additional complexity, raising questions about simplicity and administrability.

Recent legislative proposals reflect growing attention to these tax disparities, though they point in opposite directions. In 2021, Senator Wyden introduced a proposal to eliminate the in-kind redemption exemption under Section 852(b)(6), effectively bringing ETF tax treatment in line with that of mutual funds. More recently, the bipartisan GROWTH Act has proposed moving in the opposite direction by reforming RIC taxation to defer capital gains realizations until the point of sale, bringing mutual fund treatment close to that of ETFs. While both approaches would reduce differences in tax treatment across fund types, they do so through fundamentally different mechanisms and have distinct implications for investors, market efficiency, and tax revenues.

Eliminating the in-kind redemption exemption

Proposals that would repeal Section 852(b)(6) seek to equalize the tax treatment of mutual funds and ETFs by requiring both structures to recognize capital gains when appreciated assets are distributed. This approach addresses horizontal inequity by subjecting otherwise similar funds to the same realization rules.

A central concern with this approach is that 852(b)(6) plays an important role in supporting the in-kind creation and redemption process that allows ETF share prices to remain closely aligned with net asset value (NAV) throughout the trading day, as is required by the Investment Company Act of 1940. Treating in-kind redemptions as taxable events could weaken the arbitrage mechanism, potentially leading to wider and more persistent deviations between ETF prices and NAV, particularly during periods of market volatility. Critics of this approach also worry that 852(b)(6) was designed as a relief valve to prevent cascading redemptions from triggering taxable gains during periods of market stress, so treating in-kind redemptions as taxable events could exacerbate market downturns.

More broadly, eliminating the exemption would extend to ETF shareholders the same forced-realization dynamics that currently face mutual fund shareholders, leaving the underlying negative externality intact. As a result, while this approach eliminates the horizontal inequity, it does not directly address the efficiency costs associated with taxing investors based on others’ behavior.

Excise taxes and targeted reform

Compared to a full repeal of 852(b)(6), a less sweeping alternative might preserve in-kind redemptions while imposing an excise tax on the unrealized gains embedded in assets removed from a fund’s portfolio. Some argue that this approach could narrow the tax gap between mutual funds and ETFs while retaining the in-kind liquidity mechanism and raising revenue.

From a tax policy perspective, these targeted measures primarily affect the timing and distribution of tax payments rather than the structure of investor-level taxation. While an excise tax could reduce the tax advantage associated with in-kind exchange and raise revenue, it would leave unchanged the mechanisms that generate forced realizations and tax externalities for mutual fund investors. As a result, such proposals may narrow disparities across fund types without directly addressing the efficiency costs created by taxing investors based on others’ behavior.

This approach also raises administrative concerns that undermine the goal of simplifying the tax code. Implementing an excise tax on in-kind redemptions would require clear rules on when the tax is triggered, which party bears legal responsibility for remitting it, and how the tax interacts with existing arbitrage incentives. Resolving these design and compliance questions would add complexity for fund operators and tax administrators, and their treatment would play a central role in determining the effects of such proposals on investor outcomes, market functioning, and tax revenue.

Deferring capital gains until investor sales

A more comprehensive set of proposals would revise the taxation of investment funds so that capital gains are only taxed when investors sell their fund shares. Under this approach, funds would continue to pass through interest and dividend income, but capital gains realized at the portfolio level would accrue inside the fund until an investor exits their position.

From the perspective of optimal tax policy, this framework differs qualitatively from proposals focusing on altering ETF taxation. By aligning capital gains with individual investment decisions, it would eliminate the forced-realization dynamics that currently affect mutual fund holders, directly addressing the negative externality described above. It would also resolve the horizontal externality between otherwise identical investors and improve economic efficiency by allowing investor outcomes to reflect underlying risk and return rather than the actions of other shareholders. Similar approaches are used in many European countries, where fund-level capital gains are taxed only when investors sell their stake, illustrating the feasibility of taxing pooled investment vehicles at the investor level rather than annual realizations.

At the same time, deferring capital gains until investor sale would shift the timing of tax revenues. While total tax revenues over the lifetime of the investment could be higher due to higher compound returns inside the fund, revenue would generally not be collected until the investors realize their gains by selling their shares. These timing effects highlight a central tradeoff between near-term revenue needs and the potential benefits of a tax system that more closely aligns liabilities with investor behavior. On balance, however, this option offers a clearer, more administrable framework that advances equity, efficiency, and simplicity in the taxation of pooled investment vehicles.

Other considerations

Beyond changes to the tax code, some of the tax-motivated behaviors discussed above reflect the interaction of the tax rules with securities regulation rather than statutory tax provisions alone. In particular, aspects of ETF operations that facilitate tax deferral—such as the use of in-kind redemptions and heartbeat trades—are shaped by SEC rules and guidance. Regulatory changes that limit or prohibit specific practices could reduce tax-motivated behavior without altering the underlying tax treatment of investment companies. Such an approach, however, leaves broader questions of investor-level equity and efficiency to the tax code.

Step-up in basis and the permanence of deferral

A separate consideration concerns the interaction between capital gains deferral and existing rules governing realization and basis at death. Under current law, when an investor dies, the tax basis of most capital assets is adjusted to their fair market value at the date of death. As a result, unrealized capital gains accrued during the decedent’s lifetime are never subject to the capital gains tax. Heirs who subsequently sell the asset pay tax only on gains that occur after inheritance.

This rule applies across capital assets and is not specific to mutual funds or ETFs. However, it interacts meaningfully with the structural differences discussed in this paper. Because ETF investors can generally defer capital gains realization until they choose to sell their shares, long-term holders who retain ETF shares until death may permanently avoid taxation on gains realized at the portfolio level. By contrast, mutual fund investors are more likely to incur taxable gains distributions during their lifetime, even though the timing of those realizations is tied to the behavior of other investors. In this way, the combination of in-kind redemption and stepped-up basis can convert deferral into permanent exclusion for certain ETF investors.

It is important to emphasize that this outcome reflects the interaction between ETF structure and the tax treatment of capital gains at death. The step-up in basis rule predates the modern ETF and applies to stocks, real estate, and other appreciated assets. Nonetheless, the ETF structure can amplify the practical significance of step-up by allowing gains to remain unrealized at both the fund and the investor level.

Comprehensive reform of basis-at-death rules would require reconsideration of capital gains taxation more broadly and lies beyond the scope of this paper. Our focus remains on the differential treatment of otherwise identical pooled investment vehicles under current law. However, the interaction between ETF deferral and stepped-up basis further underscores how structural differences can produce materially different lifetime outcomes for economically similar investors.

Conclusion

The rise of index funds has dramatically altered the investing landscape, but not all index funds face the same tax treatment. Although mutual funds and ETFs may hold identical portfolios, differences in their tax treatment can lead to materially different after-tax outcomes for investors. In particular, current rules can cause mutual fund investors to incur capital gains based on other investors’ actions, while ETF investors are generally able to defer capital gains until they choose to sell. These differences do not eliminate tax liabilities, but they do affect the timing of taxation in ways that influence long-run investment outcomes.

The analysis in this paper highlights that these disparities raise broader concerns under widely accepted principles of good tax policy. The current system can impose different tax burdens on otherwise similar investors, create efficiency losses through forced realizations and negative externalities, and it relies on increasingly complex mechanisms to mitigate these effects. Recent efforts to equalize tax treatment through different policy approaches vary in how they address these underlying issues and in the tradeoffs they entail for investors, markets, and administration.

As index funds continue to play a central role in household saving and market capitalization, the taxation of pooled investment vehicles will remain an important policy consideration. Understanding how existing rules shape investor behavior, market structure, and the timing of tax revenue is essential for evaluating potential reforms and for assessing whether tax systems treat economically similar investments in a consistent and efficient manner.

-

Bibliography

Colon, Jeffrey M. (2023). Unplugging Heartbeat Trades and Reforming the Taxation of ETFs, University of Chicago Business Law Review 53.

Graffeo, Emily (2025, September 29). SEC Intends to Allow Dimensional to Offer Dual Share Class Funds. Yahoo Finance. (https://finance.yahoo.com/news/sec-intends-allow-dimensional-offer-161456796.html)

Goldenring, Jessica (2025). Who Stays, Who Switches: Tax Frictions and the Shift from Mutual Funds, Working Paper.

Holden, Sarah, Daniel Schrass, and Michael Bogdan (2025). Ownership of Mutual Funds and Shareholder Sentiment, 2025. ICI Research Perspective, 31(8) (November). Washington, DC: Investment Company Institute. (www.ici.org/files/2025/per31-08.pdf)

Investment Company Institute (2025). Profile of ETF-Owning Households, 2025. ICI Research Report. Washington, DC: Investment Company Institute. (https://www.ici.org/files/2025/25-etf-profiles-data.xlsx)

Kashner, Elisabeth (2017, December 18). The Heartbeat of ETF Tax Efficiency. FactSet. (https://insight.factset.com/the-heartbeat-of-etf-tax-efficiency)

Kashner, Elisabeth (2019, April 11). Heartbeats and Taxes: Don’t Let Tax Treatments Give You A Heart Attack. FactSet. (https://insight.factset.com/heartbeats-and-taxes-dont-let-tax-treatments-give-you-a-heart-attack)

Lee, Isabelle (2024, December 17). Mutual Fund Conversions Hit Record in ETF Industry’s Epic Year. Bloomberg. (https://www.bloomberg.com/news/articles/2024-12-17/mutual-fund-conversions-hit-record-in-etf-industry-s-epic-year)

Macrotrends LLC (2026). S&P 500 Historical Annual Returns (1927–2026). (https://www.macrotrends.net/2526/sp-500-historical-annual-returns)

Mider, Zachary R., Rachel Evans, Carolina Wilson, and Christopher Cannon (2019, March 29). The ETF Tax Dodge Is Wall Street’s ‘Dirty Little Secret’. Bloomberg. (https://www.bloomberg.com/graphics/2019-etf-tax-dodge-lets-investors-save-big/)

Moussawi, Rabih and Ke Shen and Raisa Velthuis (2025). The Role of Taxes in the Rise of ETFs. Review of Financial Studies 38 (10), 2988–3039.

Poterba J. M., and Shoven J. B. (2002). Exchange-traded funds: A new investment option for taxable investors. American Economic Review 922, 422–427.

Sizemore, Charles Lewis (2025, August 15). Mutual Funds Are About to Get the ETF Treatment. Here’s What It Means for Investors. Kiplinger. (https://www.kiplinger.com/investing/mutual-funds-etf-share-class-sec-ruling)

Schrass, Daniel, and Michael Bogdan (2025). Profile of Mutual Fund Shareholders, 2025. ICI Research Report. Washington, DC: Investment Company Institute. (www.ici.org/files/2025/25-rpt-profiles.pdf)

U.S. House of Representatives, Office of Rep. Beth Van Duyne (2025, March 12). Reps. Van Duyne and Sewell Lead Bipartisan Legislation to Empower Americans to Invest in Their Future. Press Release. (https://vanduyne.house.gov/2025/3/reps-van-duyne-and-sewell-lead-bipartisan-legislation-to-empower-americans-to-invest-in-their-future)

U.S. Senate Finance Committee (2021, September 10). Wyden Unveils Proposal To Close Loopholes Allowing Wealthy Investors, Mega-Corporations To Use Partnerships To Avoid Paying Tax. Press Release. (https://www.finance.senate.gov/chairmans-news/wyden-unveils-proposal-to-close-loopholes-allowing-wealthy-investors-mega-corporations-to-use-partnerships-to-avoid-paying-tax)

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

[ad_2]

Source link