Being an asset manager at Cur8 Capital brings us the added benefit of industry insights that 99% are unaware of. It’s the knowledge of these economic investment trends that asset managers use to get ahead and ensure our investors are seeing their portfolios grow.

With that said, there is no bigger asset class out there than property, and in this article, we’ll outline exactly where I think the UK property market is heading. It’s worth noting that the trends mentioned here are part of much larger global trends, so are pretty applicable across the globe.

This article will aim to cover:

- Where UK house prices are going

- Why I’m moving city as a result and where I’m going

- How Cur8 Capital will position its investments in light of these trends

How do house prices work?

In order to best take advantage of house price movements, which is intending to buy low and sell high, we first need to understand what makes a house price increase or decrease.

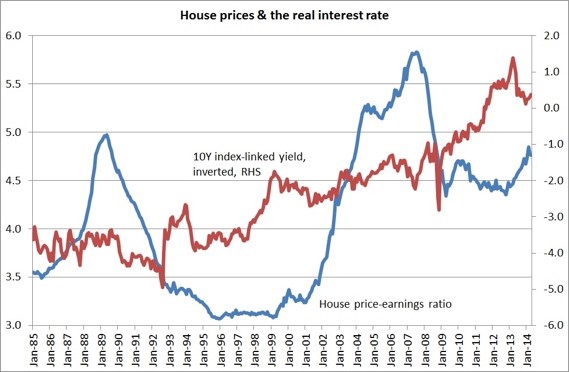

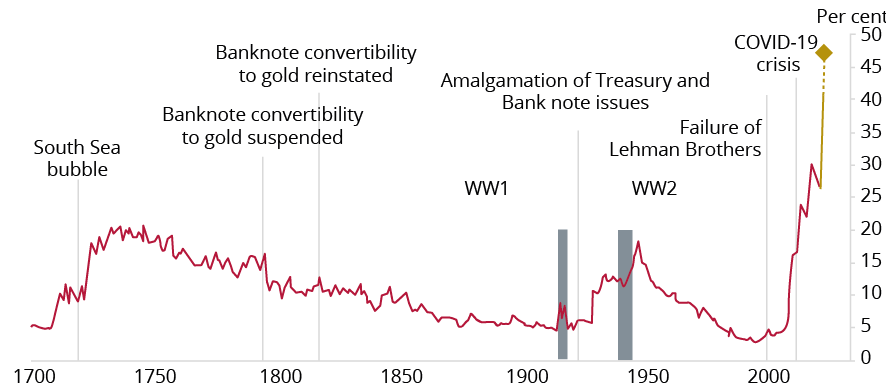

There is a conventional understanding that when interest rates go up, house prices should fall. However, as outlined in the graphs below, house prices are not really strongly linked to interest rates at all:

- Supply and demand

- Interest rates

- Money supply

Supply and demand have historically supported house prices because there is not enough supply and there is a lot of demand. This should be evident by the amount of people renting, struggling to find rental properties as well as the many people who are unable to get on to the property ladder.

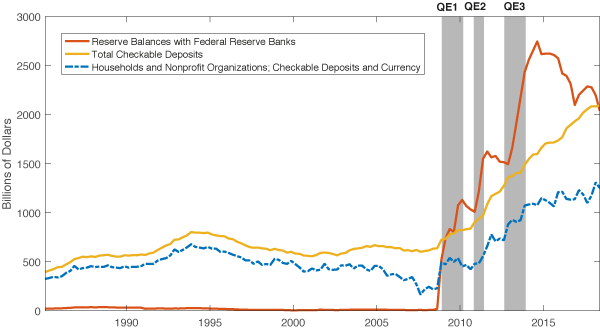

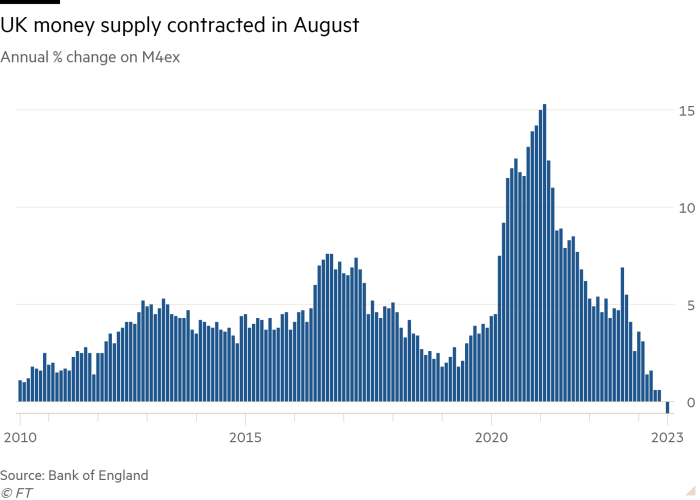

Money supply is the critical factor. Over the last 15 years, we have seen an enormous injection of capital into the economy, as outlined by this graph:

The government printed money and bought back bonds that it had issued. These bonds were held by insurance companies, pension funds and banks, and the net effect of it all was that a large amount of money came into the UK and was given to people holding these assets/closest to the money printing machine – banks, institutions, and rich people.

It is critical to understand: this money doesn’t disappear – someone ends up owning it. It is always people with the assets.

Now what the government expects to happen when it gives all this money out is that it will reduce interest rates, stimulate the economy as the banks will loan the money out and the rich people will start spending more openly.

But that didn’t happen – because interest rates were high – so both the rich and the banks were happy to hold that money and put it in low-risk investments to make a risk-free interest return on it.

So in the short-run money supply didn’t increase house prices as the money didn’t fully get deployed; however, all of that is about to change.

The piggybank is about to break

The UK money supply – i.e. the money actually in the economy started falling for the first time in years into negative late in 2023:

Rate cuts mean that the rich and the bankers’ low-risk investments won’t be making as much money anymore. Therefore, they will start shifting this huge amount of wealth into property and businesses, which make up the majority of their investment portfolios. Which in simple words means there will be a lot more money going into the real estate market, stocks and shares, and private equity over the next decade.

So in the simplest terms, I think the property market is going to start growing pretty aggressively over the next few years.

How to play this new phase of the economy

This new phase of the economy is going to create new millionaires and billionaires – and it will be people who are holding assets – stocks, property, and private equity. For the purposes of this article, we are focused on property.

The most vital piece of advice is – if you’re not on the property ladder – try your utmost to get onto it. The system is rigged, and it benefits those with assets. It is very likely that this could be the last time you are able to affordably buy a house in any of the major cities of the UK.

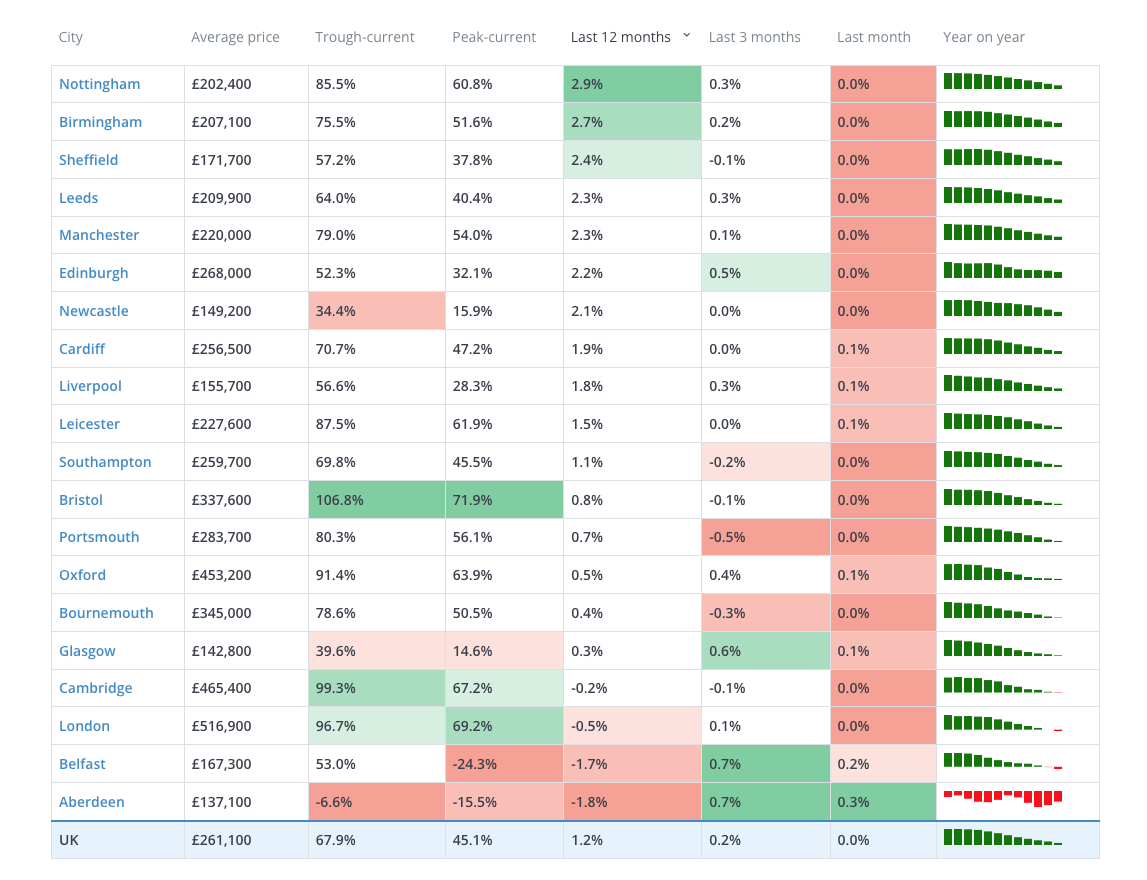

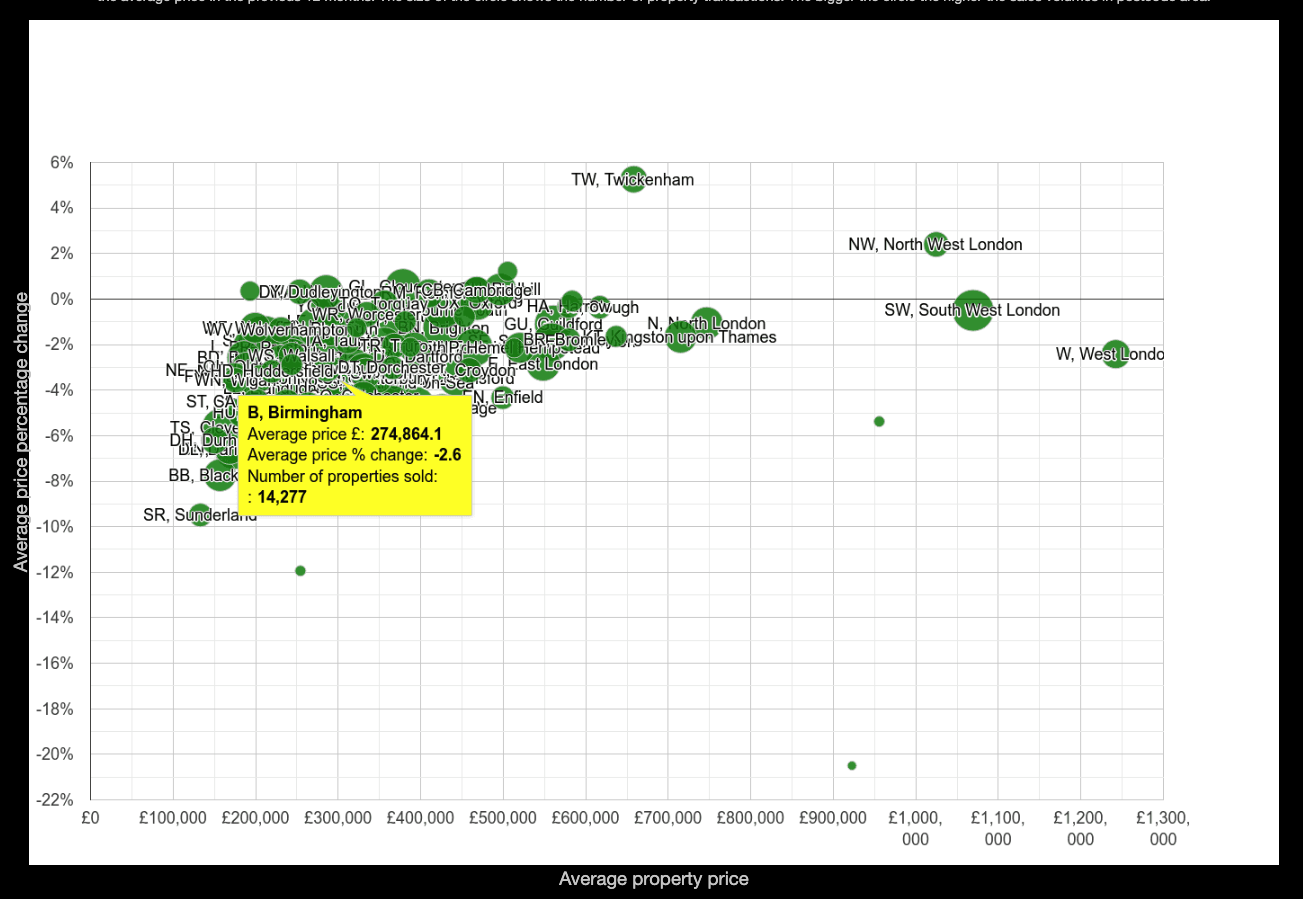

What happened to the London property market is going to happen everywhere now. This table shows this clearly:

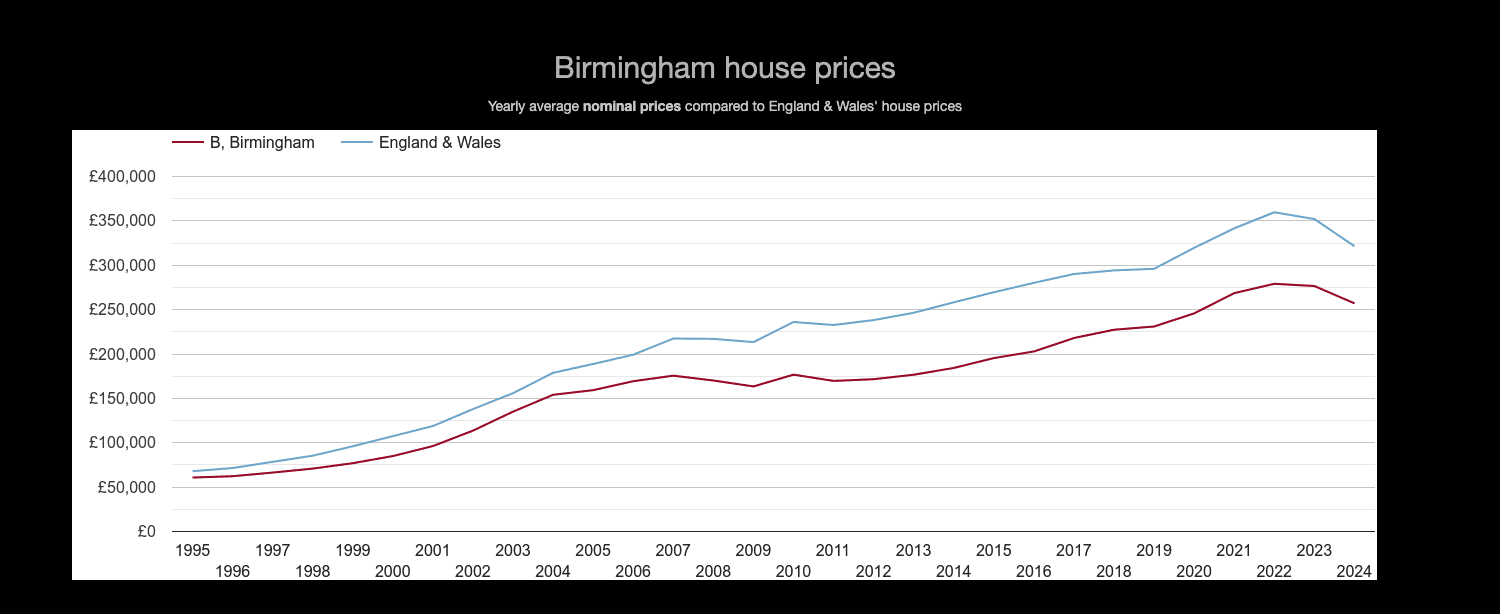

As an example, let’s look at Birmingham in particular:

And this is just a reflection that house prices are going to rise everywhere, but they are going to disproportionately rise fastest in the top cities of the UK outside of London. Why?

So the most obvious conclusion is to buy property and buy it anywhere in the top ten of this list:

Where am I moving to? Why?

I am moving to Manchester – which is one of the top five cities on that list. There’s many reasons for my decision, but among them are that the city has excellent transport links to London, and more obviously because my parents and in-laws live in or around the city.

However, from an investor’s lens, if I wanted to purchase property for income generation, then I would be investing it in flats and other rental assets in and around Manchester, Birmingham, and London. The thesis is that these assets will provide a nice yield and also appreciate over time at a higher rate than most other parts of the country for all the aforementioned reasons.

How Cur8 Capital will play this

In a recent YouTube video, we have previously addressed the megatrends we are focused on as an investment house which will inform our investment strategies – but specifically revisiting property, the key themes and areas we will be looking to exploit are:

- Serviced accommodation and blocks of flats – our marquee fund in partnership with Rasmala Bank and Viridian Apartments is very much focused on this niche and we continue to double down on this area.

- Property development – we have invested in this through bridge financing type deals already, but also deals where we are partnering up with planning-permission-seeking managers.

The area where we would love to increase our exposure with the right partners is property development.

Unfortunately, certain developers have overstretched themselves as they had been set up in a different era with lower rates – and they’ve struggled to adapt and are now running into some difficulty. So there are strong opportunities to pick up some bargains. But focusing on the long-term, there are strong margins to be made and if we are correct that house prices will rise and housing demand will remain pretty strong, then the exit is pretty clear too.

The crucial element here is the right partner though and the hunt for that continues.

Concluding Thoughts

All of the above points to one thing: Now is the best time to invest in property. The prices are only going to increase and the supply cannot keep up with the demand, so if you haven’t got your foot on the property ladder yet, then prioritise it.

If you’re interested in investing in Dubai Real Estate, then Mohsin has written a very detailed article here. And if you’re generally interested in investing in property and want to know what your options are, watch the videos we did on this subject here and here.

Finally to find out more about property investments that we offer ourselves, make a free account on Cur8 Capital, and find out more there.