Private sales accounted for a bigger proportion of the total investment.

According to a recent Knight Frank report, with the end of the year closing in, the arrival of a long-awaited interest rate cut by the US Federal Reserve (Fed) is creating a growing buzz in the investment market in the second half of 2024. In September, the Fed announced that interest rates will be lowered by half a percentage point to a targeted rate of 4.75% to 5.00%.

“In anticipation, investment activity showed some nascent signs of a pick up in September with a growth of 24.8% q-o-q to reach a total transacted value of S$8.3 billion in Q3 2024. Public sales amounted to S$2.3 billion and private sales totalled S$6.0 billion,” the report added.

Here’s more from Knight Frank:

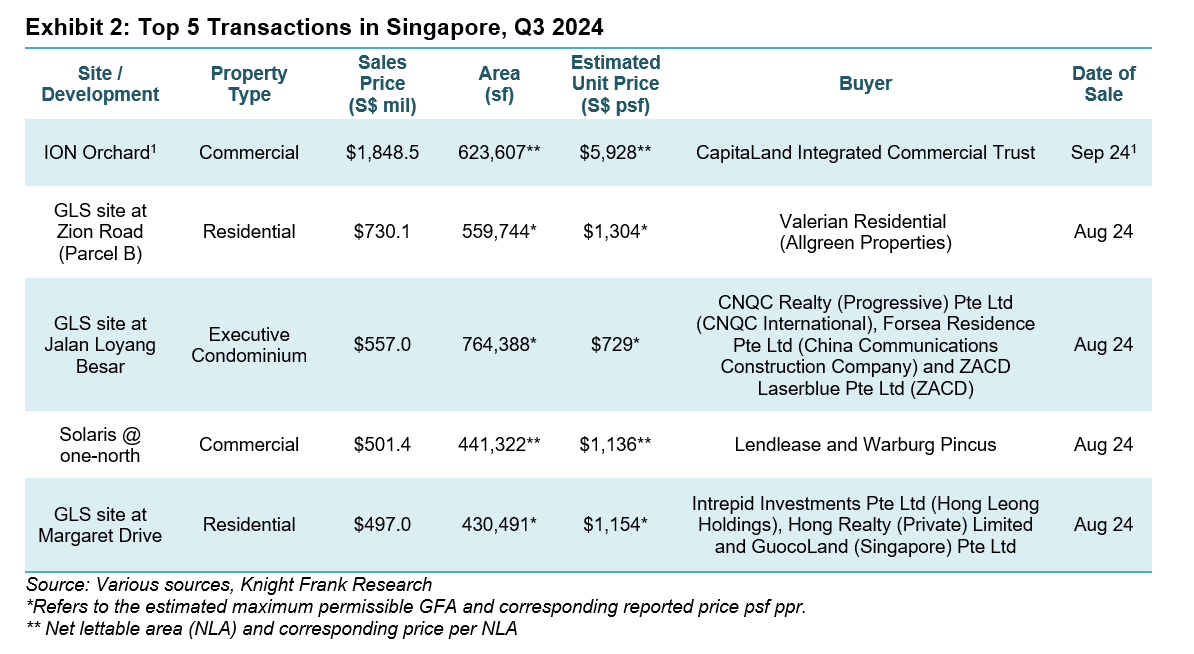

During the quarter, the total sales value of residential deals added up to S$3.2 billion, a decline of 24.7% q-o-q (Exhibit 1). Out of this total, S$2.3 billion (74.2%) comprised government land sales (GLS) sites zoned for residential use. In August, some of the GLS sites that were awarded included Zion Road (Parcel B) and Jalan Loyang Besar at S$730.1 million and S$557.0 million respectively (Exhibit 2).

In addition to these GLS sites, the sale of several good class bungalows (GCBs) located at areas such as Tanglin Hill and Belmont Road also contributed substantially to the total sales value of residential investment deals. In July, a GCB at Tanglin Hill was sold for S$93.9 million and two GCBs at Belmont Road were sold for S$73.7 million and S$57.7 million.

The acquisition of a 50% interest in ION Orchard (includes ION Orchard, ION Orchard Link, ION Art Gallery, and ION Sky) by CapitaLand Integrated Commercial Trust (CICT) from CapitaLand Investment (CLI) for S$1.8 billion in September brought the total sales value in the commercial sector to S$2.7 billion, a quarterly increase of 37.2% in Q3 2024 (Exhibit 2).

Other notable sales of retail assets included Stamford Court that was sold for S$132.0 million in August, and Sceneca Square that changed hands for S$64.0 million in September.

The biggest surge in sales activity was in the industrial sector as total sales value skyrocketed 567.6% q-o-q and 426.6% y-o-y to S$2.5 billion. This was due to the acquisition of a huge S$1.6 billion portfolio consisting of seven industrial properties by Lendlease and Warburg Pincus from a REIT owned by Blackstone and Soilbuild in August.

Several other notable industrial deals included the 51% stake sale of 20 Tuas South Avenue 14 for S$444.6 million by ESR LOGOS Reit, and the stake sale of 49% for Elementum at S$272.0 million to a sovereign wealth fund from Brunei. Both deals took place in August.