Warren Buffett is currently the tenth-richest person in the world, according to the Bloomberg Billionaires Index. In June 2024, Buffett not only estimated his net worth at more than $127 billion, but also candidly mentioned that 99% of that total was invested in a single stock: Berkshire Hathaway (NYSE: BRK.A) (NYSE: BRK.B).

Buffett acquired an ownership stake in Berkshire about six decades ago, and his considerable investing prowess has molded the company into a diversified conglomerate worth $875 billion. Under his leadership, Berkshire shares compounded at 19.8% annually between 1965 and 2023, nearly doubling the annualized return in the S&P 500 (SNPINDEX: ^GSPC) over the same period.

Buffett is undoubtedly one of the greatest minds in American business, which makes his conviction in Berkshire all the more noteworthy. Here’s what investors should know about this brilliant stock.

Berkshire has two important advantages

Berkshire Hathaway is a holding company that owns dozens of subsidiaries that fall into three segments: (1) insurance, (2) railroad, utilities, and energy, and (3) manufacturing, service, and retailing. The structure of the business is advantageous for two reasons.

First, Berkshire Hathaway is one of the largest property and casualty insurance companies in the world. As a result, it consistently generates investable cash in the form of insurance premiums. Warren Buffett explained that facet of the business in his 2009 shareholder letter.

“Insurers receive premiums upfront and pay claims later. In extreme cases, such as those arising from certain workers’ compensation accidents, payments can stretch over decades. This collect-now, pay-later model leaves us holding large sums — money we call “float” — that will eventually go to others. Meanwhile, we get to invest this float for Berkshire’s benefit.”

Buffett has invested that float to great effect over the years. Berkshire’s book value per share, a good yardstick for measuring changes in its intrinsic value, has increased at 11.1% annually over the last decade.

The second reason Berkshire’s business structure is advantageous is that many of its subsidiaries provide goods and services that are somewhat recession-proof. That is particularly true of those involved in insurance underwriting (Geico), freight rail transportation (Burlington Northern Santa Fe), and utility services (Pilot and Berkshire Hathaway Energy Company).

As a result, Berkshire Hathaway has historically outperformed the S&P 500 during bear markets, as shown in the chart below.

|

Bear Market Start Date |

S&P 500 Maximum Decline |

Berkshire Hathaway Maximum Decline |

|---|---|---|

|

March 2000 |

(49%) |

(24%) |

|

October 2007 |

(57%) |

(54%) |

|

February 2020 |

(34%) |

(30%) |

|

January 2022 |

(25%) |

(27%) |

|

Average |

(41%) |

(34%) |

Data source: Yardeni Research, Ycharts.

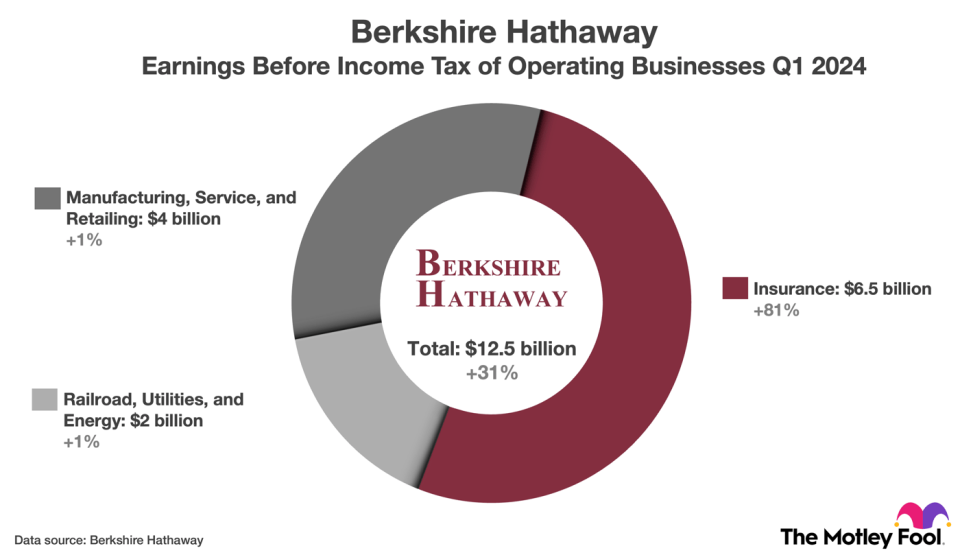

Berkshire reported solid financial results in the first quarter

Berkshire looked stalwart in the first quarter. Revenue increased 5% to $89.9 billion due to strong sales growth in the insurance and utilities subsidiaries, offset by modest sales declines across subsidiaries in other segments. Meanwhile, operating earnings before income tax increased 31% to $12.5 billion.

The graphic below shows Berkshire’s operating earnings before income tax across its three primary business segments. Importantly, those earnings do not include investment gains and losses, whether realized or unrealized. But they do include investment income, such as dividends from stocks and interest earned on U.S. Treasury bills.

Berkshire stock trades at a tolerable valuation

Going forward, CFRA analyst Catherine Seifert expects Berkshire to grow operating earnings per share at 12% annually over the next three years. That may be conservative given that operating earnings per share increased at 23% annually over the last three years. However, even accounting for that deceleration, the current valuation of 21.7 times operating earnings is tolerable.

We can also examine valuation from another perspective. Berkshire shares currently trade at 1.5 times book value. That is a slight premium to the three-year average of 1.4 times book value, but it’s not unreasonable.

Investors should not kid themselves into thinking Berkshire is cheap. But the stock kept pace with the S&P 500 over the last five years, and I think it can do the same over the next five, while offering the added benefit of outperformance during down markets.

Should you invest $1,000 in Berkshire Hathaway right now?

Before you buy stock in Berkshire Hathaway, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Berkshire Hathaway wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $786,046!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of July 2, 2024

Trevor Jennewine has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Berkshire Hathaway. The Motley Fool has a disclosure policy.

Billionaire Warren Buffett Has 99% of His Money Invested in 1 Brilliant Stock was originally published by The Motley Fool