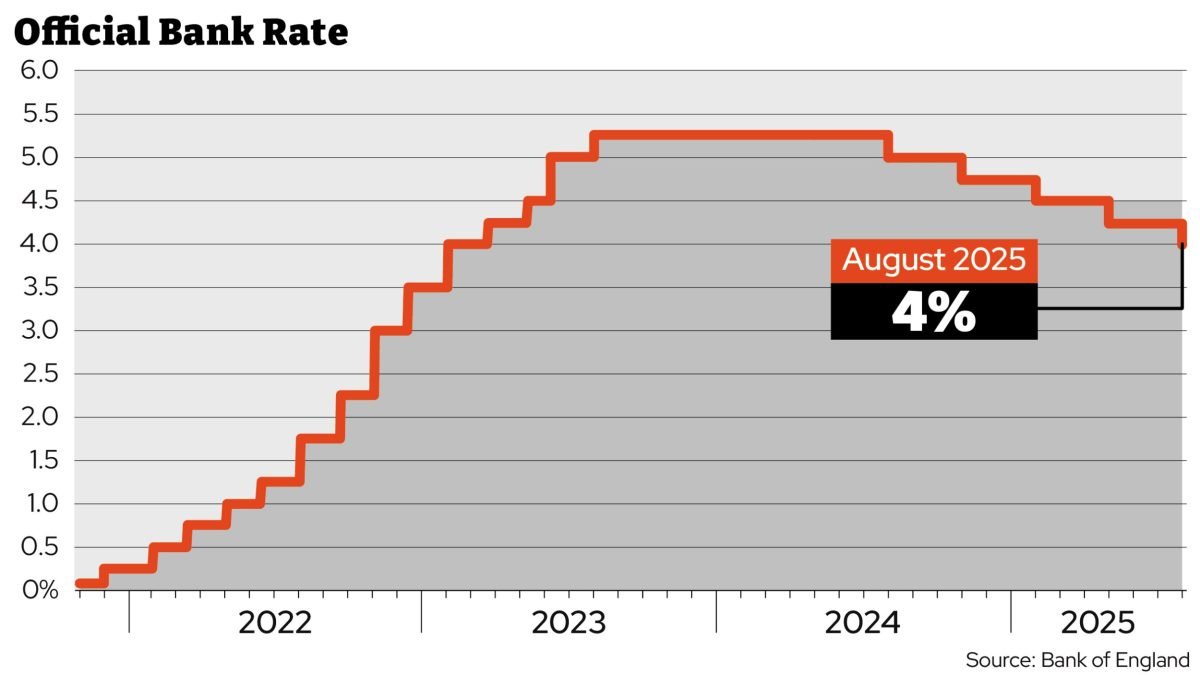

The Bank of England has cut interest rates to 4 per cent, as was widely predicted.

The Bank’s Monetary Policy Committee (MPC) voted 5-4 in favour of reducing rates from 4.25 per cent after holding them in June.

This has brought the base rate to the lowest level in two and a half years, since March 2023.

The decision required a second vote – the first time in its history – as four members initially voted for a 0.25 percentage point cut, and four voted to hold, with one member voting to reduce the bank rate by 0.5 percentage points.

A new vote was held in which that member changed their vote to 0.25, prompting the eventual result.

The move comes despite inflation standing at 3.6 per cent, well above the Bank’s 2 per cent target level.

Chancellor Rachel Reeves said: “This fifth interest rate cut since the election is welcome news, helping bring down the cost of mortgages and loans for families and businesses.”

What will happen to inflation?

Experts broadly expect inflation to remain well above the 2 per cent target for the rest of the year.

The Bank of England said it expected inflation would rise to 4 per cent in September before falling back to 2.5 per cent in 2026 and 2 per cent in 2027.

It said the return of inflation towards the target would be supported by an expected gradual reduction in food price inflation next year.

Pantheon Macroeconomics, a leading forecaster, also expects it to peak at 4 per cent in September.

It does not expect inflation to fall to 2 per cent in the next two years, and believes it will reach a low of 2.4 per cent in October 2027.

Will interest rates be cut again this year?

Economic forecasters are split as to whether there will be further interest rate cuts this year.

After August’s meeting, there are subsequent votes in September, November, and December.

Some of the more cautious forecasters predict that there may be no further reductions. Pantheon Macroeconomics, for example, assumes there will be no more cuts after August and no cuts next year.

Others expect further cuts, with Deutsche Bank forecasting reductions in November, December, and February, taking rates to 3.25 per cent.

In a note, the Bank of England said: “The restrictiveness of monetary policy has fallen as Bank Rate has been reduced. The timing and pace of future reductions in the restrictiveness of policy will depend on the extent to which underlying disinflationary pressures continue to ease.”

How will the interest rate cut affect mortgage holders?

Those on variable rate and tracker mortgages will see an imminent change in their mortgage rate as a result of the cut.

If you are on one of these deals, your mortgage will likely drop by 0.25 percentage points in the coming weeks.

According to UK Finance data, the average tracker customer owes £139,042 and is on a rate of 5.93 per cent. A typical customer on this sort of mortgage could see their payments drop by about £29 a month.

Around four in five mortgage holders are on fixed-rate mortgages, where the interest rate is locked for a set period of time, which means that if you are on this type of loan, your repayments will also not change.

Instead, you will notice a change when your mortgage comes up for renewal.

These rates are based on long-term predictions for where the base rate will go in the future. They are unlikely to be significantly affected by today’s cut because it was already expected by financial markets.

How will the interest rate cut affect renters?

Renters are not immediately affected. Some landlords may decide to increase rents by smaller amounts if their mortgage drops, while others will be fixed or own their property outright.

Rents are set by a variety of factors, including supply and demand, and so the cut is likely to have a minimal effect.

What will happen to savings rates?

Easy access savings rates can change at any point, although they tend to move depending on interest rate rises and falls, so rates may get a little lower on today’s news.

However, if you have a fixed-rate account, the interest rate is set for the period of time the account is fixed for, so it will be unaffected by the news from the Bank of England.

The best easy access savings rate on the market at the moment is Chase’s savings account at 5 per cent, though the rate includes a temporary bonus.

What does it mean for annuities?

Retirees who have defined contribution (DC) pensions – the most common type – can buy a set annual income for life in retirement with their savings.

This is known as buying an annuity, but the yearly payment you can buy with your savings fluctuates depending on several factors.

Gilt yields – the amount an investor gets for holding a government bond – are a key determinant.

Annuity providers typically buy government bonds to generate returns and high interest rates push these returns up.

So when interest rates are lower, annuity rates have also tended to be lower.

Thomas Lambert, financial planner at Quilter, said: “For retirees considering their income options, today’s rate cut could mark a turning point. Annuity rates, which have been particularly attractive in recent months thanks to high gilt yields, may start to decline.

“Anyone weighing up whether to convert part of their pension pot into a guaranteed income should take advice and consider acting sooner rather than later.”