As every investor would know, not every swing hits the sweet spot. But you want to avoid the really big losses like the plague. So take a moment to sympathize with the long term shareholders of Hartalega Holdings Berhad (KLSE:HARTA), who have seen the share price tank a massive 75% over a three year period. That’d be enough to cause even the strongest minds some disquiet.

Now let’s have a look at the company’s fundamentals, and see if the long term shareholder return has matched the performance of the underlying business.

Check out our latest analysis for Hartalega Holdings Berhad

Hartalega Holdings Berhad wasn’t profitable in the last twelve months, it is unlikely we’ll see a strong correlation between its share price and its earnings per share (EPS). Arguably revenue is our next best option. Shareholders of unprofitable companies usually desire strong revenue growth. That’s because fast revenue growth can be easily extrapolated to forecast profits, often of considerable size.

In the last three years Hartalega Holdings Berhad saw its revenue shrink by 49% per year. That’s definitely a weaker result than most pre-profit companies report. The swift share price decline at an annual compound rate of 20%, reflects this weak fundamental performance. We prefer leave it to clowns to try to catch falling knives, like this stock. It’s worth remembering that investors call buying a steeply falling share price ‘catching a falling knife’ because it is a dangerous pass time.

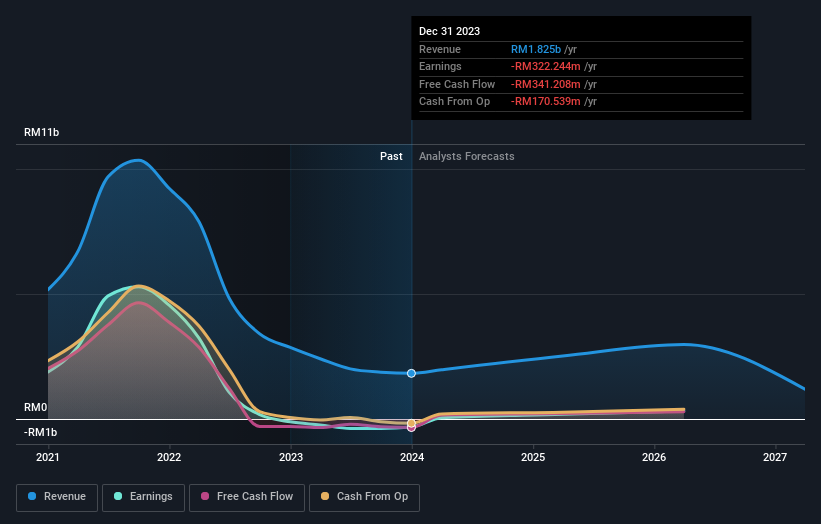

The image below shows how earnings and revenue have tracked over time (if you click on the image you can see greater detail).

It’s probably worth noting that the CEO is paid less than the median at similar sized companies. It’s always worth keeping an eye on CEO pay, but a more important question is whether the company will grow earnings throughout the years. So we recommend checking out this free report showing consensus forecasts

What About The Total Shareholder Return (TSR)?

We’ve already covered Hartalega Holdings Berhad’s share price action, but we should also mention its total shareholder return (TSR). Arguably the TSR is a more complete return calculation because it accounts for the value of dividends (as if they were reinvested), along with the hypothetical value of any discounted capital that have been offered to shareholders. Its history of dividend payouts mean that Hartalega Holdings Berhad’s TSR, which was a 70% drop over the last 3 years, was not as bad as the share price return.

A Different Perspective

We’re pleased to report that Hartalega Holdings Berhad shareholders have received a total shareholder return of 34% over one year. There’s no doubt those recent returns are much better than the TSR loss of 6% per year over five years. The long term loss makes us cautious, but the short term TSR gain certainly hints at a brighter future. You could get a better understanding of Hartalega Holdings Berhad’s growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Of course Hartalega Holdings Berhad may not be the best stock to buy. So you may wish to see this free collection of growth stocks.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Malaysian exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.