A Mint analysis of 26 companies with over 25% of their revenues from US markets in FY25 reveals a significant shift in retail investor behaviour.

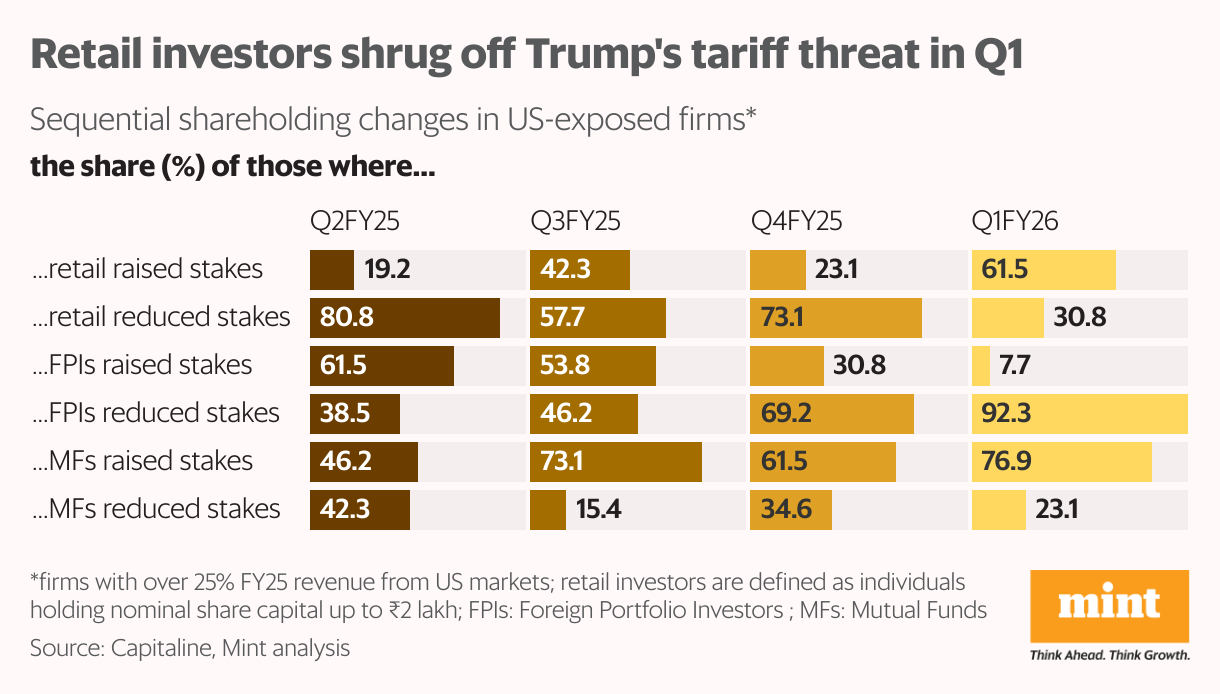

In the June quarter, 62% of these firms saw retail investors (those holding up to ₹2 lakh in equity) sequentially raise their stakes, a sharp jump from the March quarter, when only 23% of these firms witnessed a similar rise in shareholding. Individual investors have added their stakes at an accelerated pace since the September 2025 quarter.

Retail resilience

To put things in perspective, nearly 2.4 lakh new retail investors bought these stocks in the June quarter, shrugging off tariff worries. As a result, the total shareholder base in more than half of these firms—across sectors like IT, pharmaceuticals, and capital goods—rose to 12.9 million from 12.7 million in the previous quarter, according to data from Capitaline.

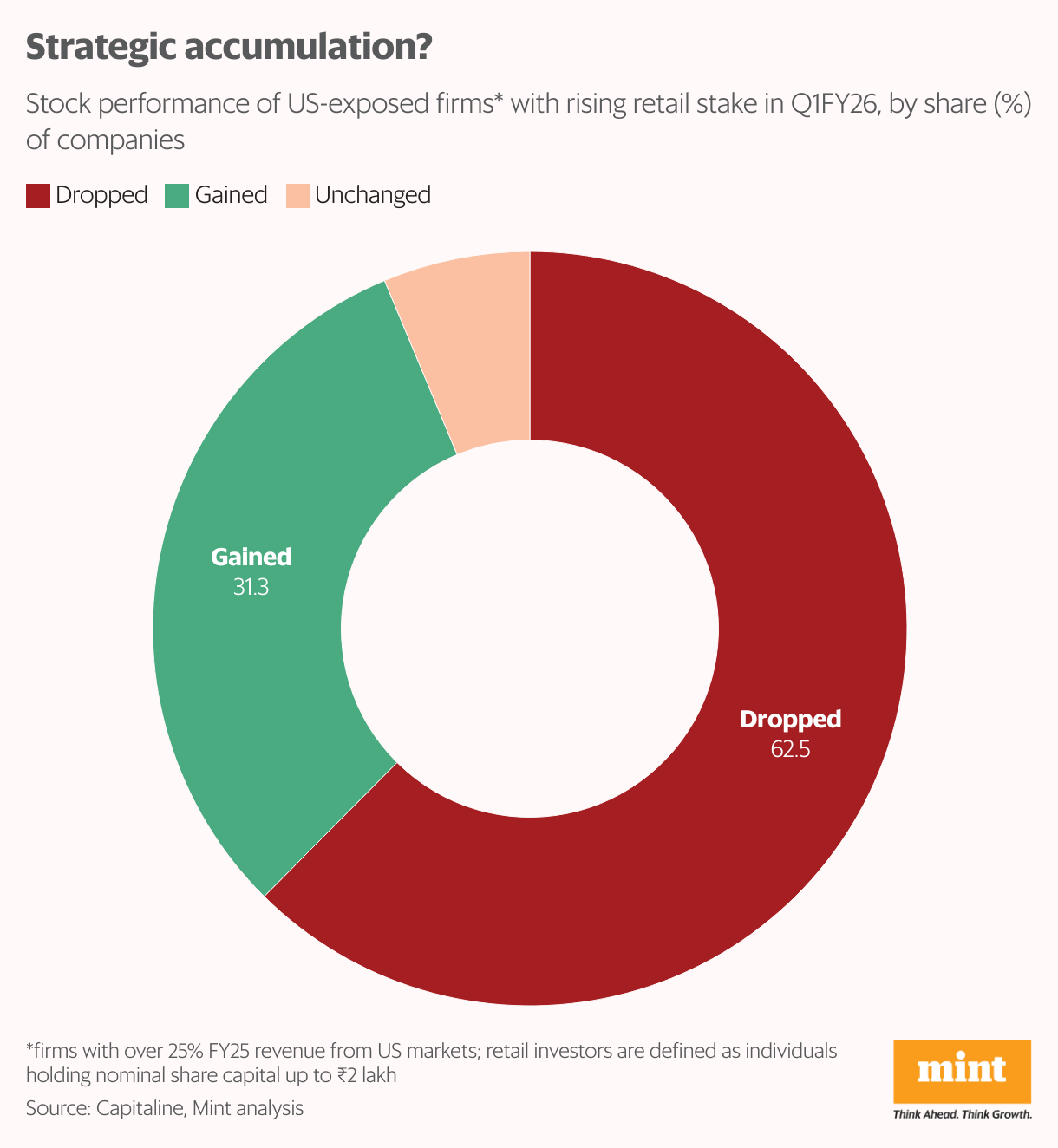

But while retail investors were busy buying, the stocks were telling a different story of steep declines, reeling under the pressures of tariff threats. Within this set, 38% saw declines of over 10% in Q1, 25% saw 1–10% fall, while only 31% managed gains of 1–12%. The rest stayed flat. This also signalled an opportunity for buying from investors.

“Domestic retail investors appear to be taking a longer-term and more structural view on US-exposed companies, focusing on the quality of businesses and secular demand rather than near-term tariff headlines,” said Sonam Srivastava, founder and fund Manager at Wright Research PMS.

“Many of these companies operate in globally competitive sectors such as IT services, pharma, chemicals, and engineering, where US markets remain the largest revenue source and pricing power, client stickiness, and high entry barriers provide resilience,” she added.

Also read: JSW Cement IPO: Can a lean, green challenger cement its place in a heavyweight market?

The divide

Meanwhile, overseas investors trimmed stakes in more than 92% of these 26 US-linked companies. However, mutual funds aligned with retail investors, increasing their holdings in 77% of these firms.

Explaining these contrarian bets, Pranav Haldea, managing director of Delhi-based Prime Database Group stated that, “retail, institutional, and foreign investors each have distinct risk appetites and investment horizons, which shape their market behaviour.”

“FPI money is typically short-term hot money—quick to exit during global crises, pandemics, or tariff concerns—while retail investors often move counter to such flows, especially when prices drop sharply. They are known to catch falling knives, often seeking short-term gains rather than holding long-term,” he added.

While FPIs may have trimmed holdings due to global risk-off flows and hedging geopolitical uncertainties, domestic investors tend to look past short-term policy risks, he added. “They bet that structural demand from the US will remain intact, and that any trade disruptions could be navigated through pricing adjustments, diversification of client bases, or negotiating trade terms over time.”

Overall, FPIs remained net buyers in Indian equities in Q1FY26, pouring in ₹43,327 crore. However, they have turned net sellers since then. Domestic institutional investors (DIIs), on the other hand, put in nearly four times ₹1.68 trillion during this period.

“Most inflows into India come from passive funds that track emerging market indices,” said Alok Agarwal, head, Quant Fund, and fund manager, Alchemy Capital. “The recent strength in the US dollar shifted money to US funds and away from emerging markets. That hurt India temporarily, but flows should return.”

Tariff tensions heat up

The surge in retail buying came against the backdrop of worsening US–India trade relations. On 2 April, Trump unveiled his sweeping “Liberation Day” tariff plan, announcing a 10% universal baseline duty on nearly all imports, alongside higher, country-specific levies for nations with trade surpluses with the US.

The baseline duty took effect on 5 April, while the targeted tariff hikes were scheduled to begin on 9 April. However, just hours before implementation, Trump announced a 90-day pause on these country-specific increases for all nations except China, leaving most countries subject only to the baseline rate.

The pause ended for India on 30 July, when Trump announced a 25% tariff on Indian imports effective 1 August, coupled with additional penalties in response to India’s continued purchases of Russian oil and military equipment. The pressure intensified on 6 August, when the US issued an executive order imposing an additional 25% penalty on select goods, effectively doubling the rate to 50%—a move that directly targeted India’s crude oil imports from Russia.

Where the buying happened

Some large-cap names with heavy US exposure stood out during the quarter. Tata Consultancy Services (TCS), India’s largest IT company, which derives more than half of its revenue from the US market, added 48,265 new shareholders in Q1FY26.

Retail investors increased their stakes by 0.7 percentage points sequentially to 3.93%, while mutual funds added a modest 0.13 percentage points to 5.13%. In contrast, foreign portfolio investors reduced their holdings by 0.56 percentage points to 11.7%.

“IT stocks like TCS, Infosys, and Wipro have fallen 20–30% since the start of the year, yet remain among India’s top 50–100 companies. Such corrections tend to attract strong retail buying, similar to their behaviour in small- and micro-cap stocks,” said Haldea.

Syngene International, the contract research subsidiary of the Biocon Group, also attracted strong retail interest. The company, which earns 61.2% of its revenue from the US, saw 17,000 new retail shareholders during the quarter, lifting retail stakes by 40 basis points (bps) sequentially to 4.33%. Even mutual funds showed confidence, raising their stake by 2.8 percentage points, while FPIs’ stakes reduced by 3.01 percentage points.

In the capital goods space, Elgi Equipments Ltd, generating 27.3% of its revenue from the US, reported steady buying from retail investors. It added 7,844 new investors, who together raised their ownership by 81 bps to 10.03%. FPIs cut their holdings by 1.44 percentage points to 28.78%, while mutual funds made small additions.

But with the threat of tariffs looming large over the entire industry, how did sentiment fare in the broader sectors where these companies fall?

In the pharmaceutical space, a Mint analysis of 178 BSE-listed pharmaceutical companies shows retail investors increased their stake in 41.6% of these firms in Q1FY26, up from 39.9% in the previous quarter.

Foreign investors were more cautious, raising stakes in only 37.6% of firms (down from 46.6%), while trimming in 48.3% (up from 43.3%). Mutual funds were largely steady, increasing holdings in 18% of companies and reducing holdingsin 12.9%.

The answer lies in the unique relationship between the two countries, experts highlight. “Over 45% of generics used in the US are sourced from India. This large interdependency makes it important for both parties to seek minimal disruption. These factors point to the likelihood of low tariff rates,” said Thomas V Abraham, research analyst at Mirae Asset ShareKhan.

Another segment at risk is information technology (IT). Retail investor interest remained strong even in information technology. Among 45 BSE-listed IT companies, 68.9% saw an increase in retail shareholding in Q1FY26, up from 57.8% in the previous quarter. FPIs added exposure in 40% of firms (up from 37.8%), while reducing in 60% (down from 62.2%). Mutual funds turned cautious, raising stakes in only 26.7% (down from 46.7%) and selling in 35.6% (up from 22.2%).

“IT is one of the sectors at risk, as tariffs on exports to the US could be imposed if Trump decides to go aggressive,” said Anand K Rathi, co-founder, MIRA Money. “However, that’s likely his last remaining weapon, and he may prefer to use it strategically—issuing warnings rather than acting immediately. While the risk is real, he may ultimately avoid it to prevent lasting damage to US–India relations.“

What lies ahead

While retail investors remain optimistic, the broader market is bracing for a decisive Q2 and Q3. Three successive quarters of weak earnings—Q3 and Q4 of FY25 and Q1FY26—have already tempered sentiment.

“If Q3 earnings again fall short, we could see sharp downgrades to overall growth projections, as the base effect alone won’t be enough to deliver the expected 14% earnings growth in FY27,” said Hemant Jain, strategist at Yes Securities. With the tariff pain far from over, how investors place their bets this quarter remains to be seen.