Consumer sentiment is near recessionary levels, the VIX recently spiked above 30, and the Fed has been cutting rates while inflation holds above target. That combination has pushed investors toward ultra-short U.S. Treasury ETFs. iShares 0-1 Year Treasury Bond ETF (NYSEARCA:SHV) has become the go-to answer for a specific question: where do you put cash when you don’t trust the market but can’t afford to earn nothing?

What SHV Is Actually Built to Do

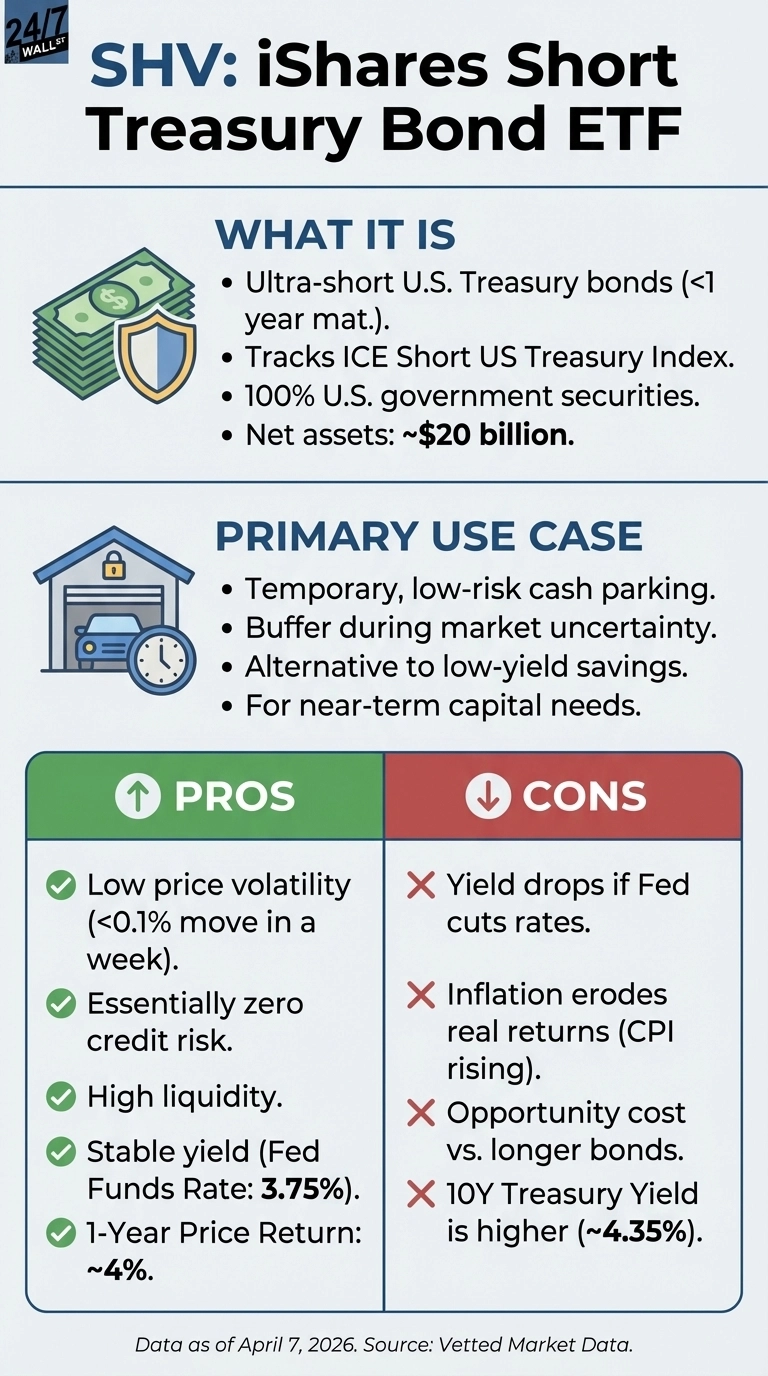

SHV tracks the ICE Short US Treasury Securities Index (a benchmark of U.S. government bonds maturing within one year), holding U.S. Treasury bonds with remaining maturities of one year or less. That ultra-short duration is the whole point. When rates move, short-duration bonds barely react in price terms, making the fund trade more like a cash equivalent than a bond fund. The return engine is simple: you earn whatever short-term Treasuries yield, minus a 0.15% expense ratio.

The fund carries no leverage and holds 100% U.S. government securities, meaning credit risk is essentially zero. With roughly $20 billion in net assets, liquidity is not a concern. Investors use SHV in three main ways: parking proceeds from a stock sale before redeploying capital, building a cash buffer during uncertain markets, and holding funds needed within the next several months without leaving them in a low-yield savings account.

On Reddit’s r/investing, discussions around short-term bond ETFs consistently return to the same logic: the tax-adjusted yields relative to principal safety make them preferable to money market alternatives for many investors. SHV fits squarely in that category.

The Rate Environment That Makes SHV Relevant Now

The Fed has cut rates three times since September 2025, bringing the federal funds rate from 4.5% down to 3.75%. Rates have held steady since December 11, 2025, suggesting the Fed has paused its easing cycle. That pause matters for SHV holders: a stable rate environment means the fund’s yield is predictable for now.

CPI has risen steadily from 320.3 in April 2025 to 327.5 by February 2026, with monthly gains of roughly 0.3% persisting into early 2026. The 10-year Treasury yield sits near 4.35%, up from the 3.97% trough seen in late February. Sticky inflation and rising long yields make further Fed cuts harder to justify, keeping short-term rates elevated and SHV’s income competitive.

Does the Fund Deliver on Its Promise?

By its own terms, yes. SHV returned nearly 4% over the past year, with a current share price near $110. The fund moved less than 0.1% in a single week and under 0.3% over the past month, even as the VIX spiked to 31 in late March. That stability is exactly the product.

The five-year picture shows the tradeoff clearly. SHV’s cumulative five-year return is about 17%, driven entirely by yield capture rather than price appreciation. A broad equity index delivered multiples of that over the same window. The relevant comparison is cash sitting idle, not the S&P 500.

Consumer sentiment reinforces why investors are reaching for instruments like this. The University of Michigan Consumer Sentiment Index sits at 56.6, well below the 80-point neutral threshold and near levels historically associated with recessionary psychology. When investors feel that pessimistic, they want somewhere safe to wait, and SHV offers yield without forcing them to take on duration or credit risk.

Three Real Tradeoffs Worth Understanding

- Rate sensitivity works both ways. SHV’s yield tracks short-term rates closely. If the Fed resumes cutting, the fund’s income will decline in step. With markets pricing in the possibility that further cuts may not arrive until late 2026 or beyond, the near-term yield looks stable, but investors expecting today’s yield to persist indefinitely will be disappointed if the rate environment shifts.

- Inflation erodes real returns. The fund’s nominal return is meaningful, but with CPI rising steadily through early 2026, real purchasing power gains are thin. SHV preserves nominal capital well; it does not protect against inflation the way TIPS or commodities might.

- Opportunity cost accumulates over time. The 10-year Treasury yield near 4.35% means investors can earn more by extending duration, and the 10Y-2Y yield curve spread of about 0.5% shows the yield curve is no longer inverted. Investors who stay in SHV indefinitely are leaving yield on the table compared to slightly longer-duration alternatives.

SHV is the right tool for investors who need a temporary, low-risk home for capital they plan to redeploy. Anyone treating it as a long-term holding will find that yield compression and opportunity cost quietly erode the case for staying.