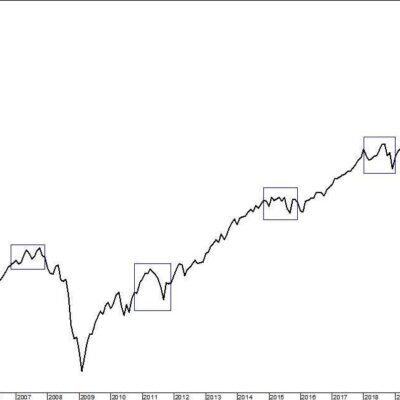

Geopolitical risks have been on the rise recently, posing a growing number of challenges for investors trying to navigate the current environment.

The recent developments, such as the recent gains by fringe parties in the UK and French elections, “have underlined that political outcomes are becoming harder to predict,” UBS strategists said in a recent note. Moreover, the ongoing conflicts in Gaza and the prolonged Russia-Ukraine war add to the uncertainty.

Despite these challenges, UBS strategists advise against exiting risk assets. Historical data shows that market impacts from international disputes are typically short-lived. UBS notes that electoral shifts, like those in India or France, often result in volatility rather than sustained downturns.

For example, since the attack on Pearl Harbor, the S&P 500 has been higher two-thirds of the time twelve months after the start of a crisis, UBS highlighted.

Even with persisting geopolitical risks, the MSCI All-Country World Index has risen 14% so far in 2024. UBS warns that selling in response to immediate uncertainties can be counterproductive, locking in temporary losses and missing out on market recoveries.

Instead, to navigate the current uncertainties, the bank’s team recommends building resilient portfolios. A well-diversified portfolio can reduce volatility from geopolitical conflicts and electoral uncertainty.

“Structured strategies can enable investors to retain exposure to further potential gains in stocks, while reducing sensitivity to a correction.”

In a separate report, UBS maintained its core investment views this month, despite the recent market rotation from large-cap tech stocks into small-caps.

The bank continues to recommend that investors position for lower rates, seek quality growth stocks, and seize the AI opportunity. According to UBS, the data needs to be great, not just good, for the rotation to continue—specifically, immaculate disinflation with growth above trend.

July has seen a marked reversal across equity markets. The leaders from the first half of the year have become the relative losers this month, while previous laggards have surged.

The Nasdaq 100 is down 0.6% in July after rising 16.7% in the first half of 2024. Similarly, the S&P 500 has returned 0.8% in July after gaining 15% in the first half of the year. In contrast, the Russell 2000 small-cap index is 7.6% higher in July, following a modest 0.9% increase in the first half of 2024.