Amid conflict in the Middle East, investors see geopolitical tensions rising. That can often prompt shareholders to reduce stock holdings or at least hold off on buying shares. Restraint could be a wise move, as it is too early to tell if or how much the events abroad will affect the market.

Amid a possible bear market, now is a good time to compile a wish list of stocks to buy should prices fall. These names could serve investors well if they can buy at a considerable discount.

Image source: Getty Images.

Costco

One cannot blame investors for looking at Costco (COST 3.25%) stock and wondering, “is the opportunity over?” The company has built a consistent track record of rising sales and profits and has also steadily expanded, both domestically and abroad.

Its members pay annual membership fees that allow them to buy high-quality, bulk goods at competitive prices. Since it also sells groceries and other necessities, the company is recession-resistant, and annual sales declines are rare.

In the first six months of fiscal 2026 (ended Feb. 15), its $137 billion in revenue grew 9% compared to year-ago levels. That was above the 6% increase in fiscal 2025. With that, the $4 billion in profit in the first half of fiscal 2026 surged 13% higher, surpassing the 10% yearly growth in fiscal 2025.

Today’s Change

(-3.25%) $-33.56

Current Price

$998.47

Key Data Points

Market Cap

$443B

Day’s Range

$995.50 – $1029.00

52wk Range

$844.06 – $1067.08

Volume

2.3M

Avg Vol

2.1M

Gross Margin

12.93%

Dividend Yield

0.52%

While growth has remained relatively steady, the growth rates arguably do not justify its 53 P/E ratio. The earnings multiple has rarely fallen below 40 over the last five years.

Still, in the previous decade, the P/E ratio sometimes dropped below 30. That history indicates that if investors buy Costco stock for under 30 times earnings, they could earn market-beating returns with minimal risk.

Dutch Bros

Dutch Bros (BROS +0.05%) is a coffee chain that has expanded rapidly and steadily risen in popularity. Customers have taken to its “broista” culture, which it created to improve the customer experience. Also, they can choose from a variety of coffees and other beverages, all of which help it to stand out in a competitive market.

Additionally, it is in the middle of the same kind of regional to national expansion that caffeinated Starbucks‘ growth in past years. Dutch Bros’ 1,136 locations at the end of 2025 were up from 982 in the previous year. From there, it intends to open 2,029 locations by 2029 and grow beyond that point.

In 2025, revenue of more than $1.6 billion surged 28%, including a 5.6% rise in same-shop sales. That more than doubled its net income over the same period to nearly $80 million.

Today’s Change

(0.05%) $0.03

Current Price

$55.88

Key Data Points

Market Cap

$9.2B

Day’s Range

$54.88 – $56.75

52wk Range

$44.58 – $77.88

Volume

2.4M

Avg Vol

5M

Gross Margin

25.68%

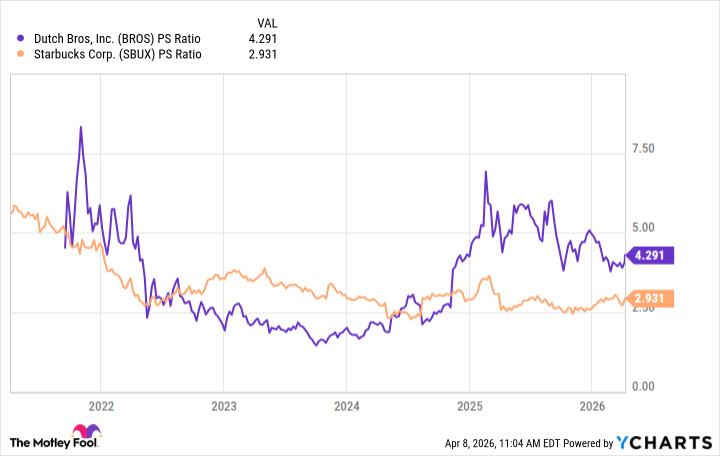

Such growth has helped boost the consumer discretionary stock to a P/E ratio of 84. Still, investors have a glimmer of hope as its 4.3 price-to-sales (P/S) ratio has fallen in recent months.

BROS PS Ratio data by YCharts

That is above the Starbucks P/S ratio of 2.9. However, when Dutch Bros’ sales multiple has fallen below Starbucks’ in the past, a surge in the stock price has followed. If that inversion happens again, past stock behavior suggests that Dutch Bros investors could earn market-beating returns.