NatWest (NWG.L) and Halifax have increased mortgage costs after the Bank of England kept interest rates on hold.

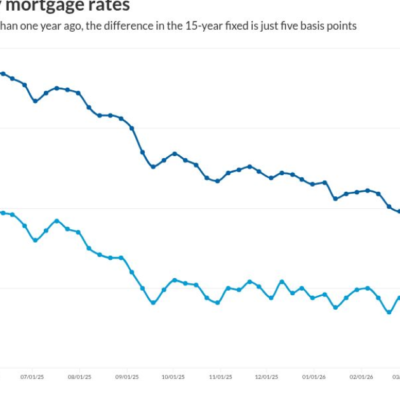

The average rate for a two-year fixed mortgage came in at 4.53% this week, unchanged from the previous week, according to data from Uswitch.

The average five-year fixed deal came in at 4.94%, lower than last week’s 4.98%. These are the average rates across all lenders for a 75% loan-to-value (LTV) mortgage, meaning buyers need a down payment of at least 25% of the purchase price.

The Bank of England has left interest rates on hold at 3.75% as expected, but most lenders decided to hike mortgage costs before the decision, with NatWest (NWG.L) and Halifax following this week.

Higher mortgage costs come as some 5,160 homeowner mortgaged properties were repossessed last year, marking a 39% jump compared with 2024, according to figures from a banking and finance industry body. In 2024, 3,710 homeowner mortgage repossessions took place.

Read more: UK economy posts sluggish 0.1% growth in final quarter of 2025

Despite the annual increase, overall repossession numbers remain lower than long-term averages, the report said.

The annual total for 2025 is significantly lower than the 44,100 homeowner repossessions that occurred in 2009, amid the fallout from the financial crisis.

In the fourth quarter of 2025, 1,210 homeowner repossessions were recorded, marking a 17% increase compared with the same period in 2024, but 13% lower than the number of homeowner repossessions in the previous quarter.

Looking at mortgage arrears, 80,490 homeowner mortgages were in arrears of 2.5% or more of the outstanding balance in the fourth quarter of 2025. This was 4% lower than the previous quarter and 13% lower than in the same period in the previous year.

Here’s more detail on major lenders’ mortgage rates this week:

HSBC (HSBA.L) has a 3.76% rate for a two-year deal, with a £999 booking fee, which is unchanged from the previous week. For those with a premier standard account with the lender, this rate is 3.73%.

Looking at the five-year options, the fixed standard rate is 3.88% with a £999 fee, which is also unchanged.

Both cases assume a 60% LTV mortgage, meaning buyers need a deposit of at least 40%.

HSBC (HSBA.L) offers 95% LTV deals, meaning you only need to save for a 5% deposit. However, the rates are higher, with a two-year fix at 4.74% or a five-year fix at 4.79%.

This is because their financial situation and deposit size determine the rate someone can get. The larger the deposit, the lower the LTV, allowing buyers to access better deals because lenders consider them less risky.

Read more: The UK’s most affordable city for single homebuyers

The lender has recently unveiled a cashback offer of up to £2,000 to ease the upfront costs of entering the housing market.

The bank’s enhanced incentive package, which brokers say could ignite a fresh round of competitive pricing among high-street lenders, marks one of the most generous cashback schemes currently available. The measure is aimed at supporting borrowers struggling with deposit and moving costs at a time when affordability pressures remain high despite a recent easing in mortgage rates.

NatWest’s (NWG.L) two-year deal has jumped from 3.59% to 3.70%, with a £1,495 product fee, a figure that sits very close to last week’s 3.73% five-year deal.

The cheapest five-year fixed deal is 3.85%, also higher than last week’s offer. In both cases, you’ll need a deposit of at least 40% to qualify for the rates.

Barclays (BARC.L) has a two-year fix available at 3.65% with a £899 product fee, which remains the same from last week. The five-year deal is also untouched at 3.90%.

Barclays (BARC.L) launched 95% loan-to-value (LTV) mortgages for purchasers of new-build houses, in a move aimed at easing the path to home ownership, especially for first-time buyers.

The offer applies to new-build houses with a maximum purchase price of £600,000. Previously, buyers were required to pay a 10% deposit, meaning a £60,000 deposit on a £600,000 property. Under the new criteria, that requirement could be halved to £30,000.

Earlier in the year, Barclays (BARC.L) launched a mortgage proposition to help new and existing customers access larger loans when purchasing a home.

Read more: Best credit card deals of the week

The initiative, known as Mortgage Boost, enables family members or friends to effectively “boost” the amount that can be borrowed toward a property without needing to lend or gift money directly or provide a larger deposit.

Under the scheme, a borrower’s eligibility for a mortgage can increase significantly by including a family member or friend on the application. For example, Barclays (BARC.L) stated that an individual with a £37,500 annual income and a £30,000 deposit could borrow up to £168,375, meaning the most they could afford would be a home worth £207,375.

However, with Mortgage Boost, the total borrowing potential can increase if a second person, such as a parent, is added to the application. In this case, if the second applicant also earns £37,500 a year, the combined income could push the borrowing limit to £270,000, enabling the buyer to afford a home worth up to £300,000.

Nationwide (NBS.L) has a two-year fix at 3.82% for first-time buyers, which is the same as before. For a five-year deal, the rate is 4.16%, also unchanged. Both deals require a 40% deposit and come with a £999 upfront fee.

First-time buyers also receive £500 cashback when they complete their mortgage with Nationwide (NBS.L).

The lender this week announced an expansion of its high loan-to-income (LTI) lending, a change that could see some borrowers access tens of thousands of pounds more than previously available.

Under the new terms, home movers and customers remortgaging will now be able to borrow up to six times their annual income. This enhanced offering extends to both new and existing customers moving home or remortgaging, and applies to loans with a loan-to-value (LTV) up to 95%.

Read more: UK housing market showing early signs of recovery, surveyors say

To qualify for this increased borrowing, sole applicants must demonstrate a minimum annual income of £75,000, while joint applicants must demonstrate a minimum yearly income of £100,000. These income thresholds remain consistent with previous requirements, which allowed eligible groups to borrow up to 5.5 times their income.

The changes mean that, for example, a sole applicant who was a new customer moving home or remortgaging, with an income of £75,000, may previously have been able to borrow up to £412,500 from Nationwide (NBS.L). But now they could potentially borrow up to £450,000 — an increase of £37,500.

Nationwide (NBS.L) has also become the first lender to allow a mortgage deed to be signed electronically and without the need for a witness in a “significant step” for the market.

Anyone purchasing a property or looking to remortgage with Nationwide (NBS.L) will be able to sign their mortgage deed electronically if their solicitor is set up to use a Qualified Electronic Signature.

Halifax, the UK’s largest mortgage lender, offers a two-year fix at 3.91% (also 60% LTV), which is more than last week’s 3.72%.

The lender, owned by Lloyds (LLOY.L), also offers a five-year rate of 4.02%, also higher than last week’s 3.88%.

It has a 10-year deal with a mortgage rate of 4.87%.

Santander (BNC.L) withdrew its 60% LTV mortgage products for first-time buyers on borrowing of less than £250,000 on two- and five-year terms on 19 September.

A spokesperson for the bank said that the “change was part of a reprice following the changes to swaps after the Bank of England held interest rates”.

Santander (BNC.L) continues to offer products with LTVs of 85% or above for first-time buyers, with the cheapest two-year fix at 4.10% and the cheapest five-year fix at 4.23%.

For home movers with a 40% deposit, Santander (BNC.L) is now offering a two-year fixed rate of 3.51% and a five-year deal of 3.73%, a hike from the previous 3.72% deal.

The lender has launched a mortgage that lets first-time buyers borrow up to 98% of the property’s value.

The deal does require a minimum £10,000 deposit, though, so borrowers would need to be purchasing a home for £500,000 to have put down a deposit as low as 2%.

Read more: Six common remortgaging mistakes to avoid

Santander UK (BNC.L) said its “my first mortgage” deal has a fixed rate of 5.19% over five years and has no product fee.

The product, with up to 98% loan-to-value (LTV), is available for maximum lending of up to £500,000, repayable over a term of 5-40 years.

The deal is not available to self-employed applicants and covers only applicants living in Britain, with Northern Ireland excluded, Santander (BNC.L) said.

It is available for a minimum of £190,001 being borrowed, and £250 cashback is payable on completion.

Lending above 95% and up to 98% is available on existing houses only, Santander said.

All lending also remains subject to Santander’s (BNC.L) broader affordability checks, including a maximum loan-to-income multiple of 4.45 times salary.

Barclays (BARC.L) offers the most competitive two-year deal on the market for first-time buyers, with a fixed rate of 3.65%. When it comes to a five-year fixed deal, NatWest (NWG.L) takes the crown, with its 3.85% offer. However, any of these deals requires a hefty 40% deposit.

With the average UK house price at £297,755 in December, prospective homebuyers would need a deposit of around £120,000 to secure the cheapest rates.

A growing number of homeowners in the UK are opting for mortgage terms of 35 years or longer, with a significant rise in older borrowers stretching their repayment periods well into their 70s.

Skipton Building Society is allowing first-time buyers to borrow up to 5.5 times their income, helping more borrowers get on the housing ladder.

Leeds Building Society reduced the minimum household income requirement on its first-time-buyer mortgage range. This means single or joint first-time buyer applicants with a household income of £30,000 may now be able to borrow up to 5.5 times their earnings.

Mortgage holders and borrowers have faced higher repayments in recent years, as the BoE’s higher base rate has been passed on by banks and building societies.

Many homeowners will hope the Bank of England continues to cut interest rates. At the same time, savers will likely root for rates to remain at or near their current levels.

Read more:

Download the Yahoo Finance app, available for Apple and Android.