[ad_1]

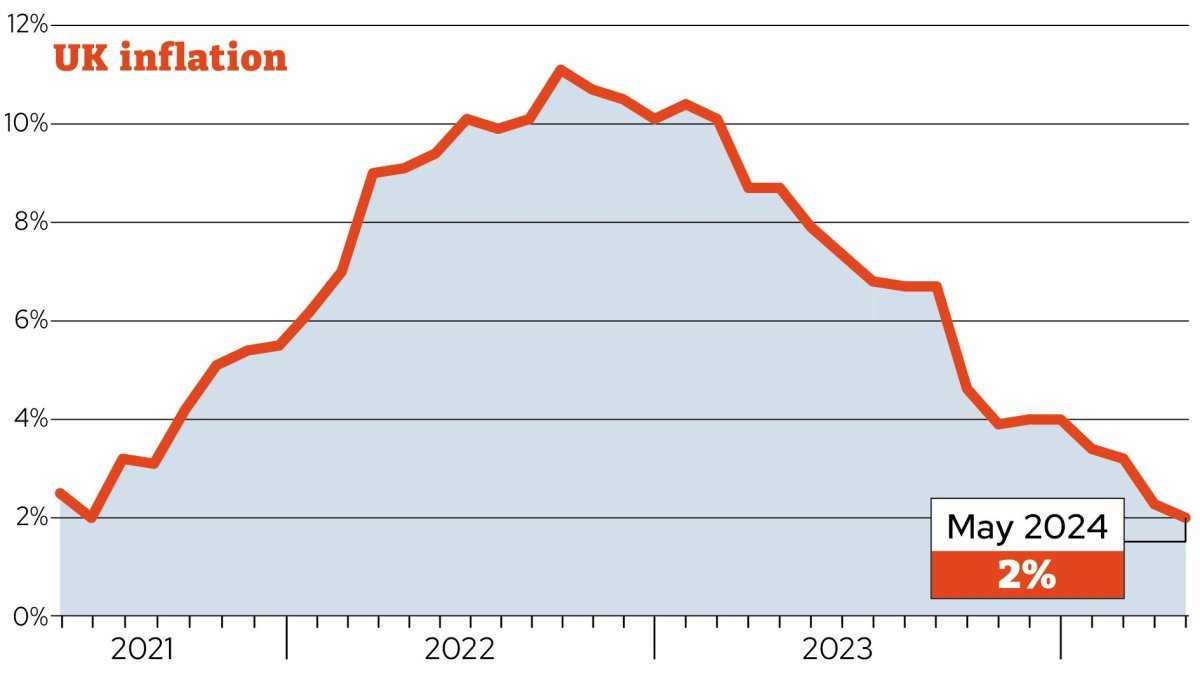

Inflation fell to 2 per cent in the year to May, which is the Bank of England’s target level. It is the first time it has reached this since July 2021.

This is down from 2.3 per cent in April, figures released on Wednesday by the Office for National Statistics (ONS) show.

Inflation has been falling consistently this year, following a peak of 11.1 per cent in 2022.

It comes the day before the Bank of England makes a decision as to whether the base rate will stay the same, at 5.25 per cent, or if the Monetary Policy Committee (MPC) will finally cut them.

What is predicted to happen to inflation in 2024?

Inflation is expected to fall further later this year, although many experts have warned it will then rebound and go back above the target.

The Bank of England’s Monetary Policy Committee (MPC) warned in a report recently that the inflation figure would increase slightly to around 2.5 per cent in the second half of 2024.

The major reason for this is that inflation is measured based on the growth in prices over the past year, so a large part of the figure is based on what prices were 12 months ago.

This April, the energy price cap – the maximum most households pay for each unit of gas or electricity used – was cut by the regulator Ofgem.

By comparison, in April 2023, the amount people were paying for their energy was at the highest level on record.

Energy prices started to fall in the second half of 2023, and experts are not currently expecting more dramatic cuts. This means that once we reach the second half of 2024, the annual price fall in energy will not be as dramatic as it is in current figures, which means it won’t have as big a downwards drag on the overall inflation figure as it’s currently having.

What does this mean for interest rates?

The Bank of England tends to cut interest rates as inflation comes down. At its next meeting tomorrow, most experts predict that the Bank will hold rates at 5.25 per cent while others think it could finally cut them.

“We think the MPC will vote 7-2 to keep Bank Rate on hold at 5.25 per cent, the same vote split as in May. We also expect rate-setters to leave their guidance on the timing of the first rate cut little changed,” experts from Pantheon Economics said.

A note released by Deutsche Bank Research added: “We expect the MPC to keep the Bank Rate at 5.25 per cent – marking its seventh consecutive meeting where policy has remained unchanged.

“Despite upside surprises to inflation and wage growth, we expect a 7-2 vote tally with external MPC member Swati Dhingra and Deputy Governor Dave Ramsden voting for a quarter point rate cut.”

Meanwhile, a report from economists at BNP Paribas, said: “We expect the Bank to keep Bank Rate on hold at its 20 June meeting by an unchanged vote split of 7-2 with broadly similar guidance.”

What does this mean for mortgages, savings and pensions?

Mortgages

Mortgages are not directly affected by inflation, although many products are affected by the Bank’s base rate, which inflation influences.

Tracker products and standard variable mortgages change directly when interest rates change.

Fixed mortgages tend to work on long-term predictions for where the base rate will go. This means that a big drop in inflation can send mortgage rates down, because it can lead experts to believe the base rate will fall sooner rather than later.

Today’s drop is likely not dramatic enough to trigger a plunge in rates but will still be welcome news for homeowners.

Savings

High inflation is bad news for savers as it erodes the value of money held in the bank. Therefore, the lower the rate, the better the news for savers.

However, experts believe we are “past the peak” for savings with most fixed rates now dropping below 6 per cent. This means it is worth taking advantage of the best deals now.

Currently, the best easy-access account is 5.02 per cent with Oxbury Bank – above inflation. The best one-year fixed is with Hodge Bank at 5.16 per cent.

Pensions

The drop in inflation will be welcomed by pensioners who have been struggling with the cost of living crisis over the past two years, especially those for whom the state pension makes up a large portion of their income.

Another factor to be aware of is the impact of inflation on annuity rates.

Annuities offer a guaranteed annual income in retirement. They offer an alternative to drawing down money from a pension pot, which could eventually run out, particularly if a retiree lives longer than expected.

While they have been unpopular in recent years, rising interest rates have improved the annual incomes someone can buy.

But for retirees opting for one, time may be of the essence. As inflation goes down, the Bank of England is likely to cut interest rates later this year, so today’s good rates may not last indefinitely.

[ad_2]

Source link