[ad_1]

Image source, Nicola Webb

- Author, Lora Jones

- Role, Business reporter, BBC News

Young homebuyers are facing huge challenges when it comes to getting on – and staying on – the housing ladder.

Nicola Webb, a 34-year-old nurse, felt she had little choice but to opt for an ultra-long mortgage when purchasing her first home last year.

It’s set to end when she is 68, but she says stretching out the repayments is “the only way I can just about afford my mortgage as a single homeowner”.

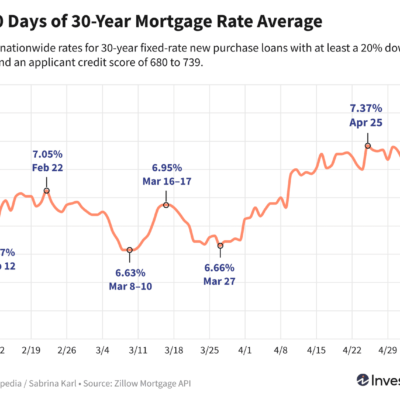

“I’ve not known lower mortgage rates so I just accept what it is.”

Despite the fact that she managed to save a chunky deposit for her £147,000 two-bedroom flat in Gloucestershire, Nicola’s five-year fixed rate mortgage costs £598 a month – about a third of her monthly wages after tax and student loan deductions.

Once her student loan is paid off – or eventually written off – she hopes to reduce the length of her mortgage term from 35 years, or look at using any extra disposable income to overpay it.

She says she’s grateful she has been able to get on the housing ladder at all. While mortgage costs take up a large part of her income, she thinks it is still cheaper than renting in her local area.

“I was having no luck at all with renting… and for me it’s all about trying to keep it as cheap as possible.”

Recent figures suggest that Nicola’s situation is becoming more and more common.

Data from the Bank of England shows that hundreds of thousands of homeowners have taken out mortgages in the last three years that they will still be paying off into retirement.

While longer mortgage terms might make repayments more affordable in the here and now, homeowners will be paying off more overall in interest.

Some industry figures have also expressed concern that buyers may not be able to afford a mortgage once they retire and will raid their pension savings to clear their home loan, leaving them with less to live on in old age.

But for some, a longer term of 35 or 40 years is seen as a temporary solution as they wait to see if mortgage rates will fall back from relative highs.

Martin Tapper, a mortgage broker based in Essex, told the BBC that most of the first-time buyers he has advised this year have opted for 40-year terms.

“A young family can escape exorbitant rent costs in order to purchase a home where the mortgage cost is far cheaper on a longer term,” he suggests.

He adds he would only guide a client to these longer terms if they were the “right kind”, saying he always recommends switching back to a shorter term later on if possible, for example if a client’s wage has gone up or if they’re moving home.

And, he says, it is vital to get insurance to protect against payments becoming tricky if someone’s health deteriorates or they lose their job.

For 30-year-old Shane Lees, weighing up the pros and cons of an ultra-long mortgage has been a serious undertaking.

He and his partner are remortgaging so that they can buy a three-bedroom house in West Sussex where they can start a family.

After speaking to six or seven mortgage brokers, they have decided to choose a mortgage term of 35 years, with the hope of dropping down to 25 years at the end of a two-year fixed deal.

Shane says that it would be “affordable, but deeply uncomfortable” if they wanted to purchase a property at the top end of their budget on a 25-year-term.

He feels a longer mortgage term at about 5.5% seems like the “most sensible option right now”, if he and his partner manage to find a property valued at about £370,000.

The pressure faced by younger homeowners like Shane is pretty clear, with the sharp rise in the proportion of mortgages that run beyond state pension age.

The number of homeowners aged under 30 taking out such mortgages more than doubled over the two-year period, while for those aged under 40 the number was up 30%.

But Sarah Coles, head of personal finance at Hargreaves Lansdown, says people shouldn’t bank on interest rates being lower when they come to reduce the term later.

“Economists are constantly changing their expectations for when the Bank of England will cut rates.

“Back in January some of them were predicting cuts as early as March, and now we’re expecting them this summer instead. Even then, cuts aren’t expected particularly rapidly, so anyone holding their breath for much lower rates will have quite a wait on their hands.”

She suggests that those on a 35 or 40-year mortgage need not only a plan in place to pay it off, but also a plan B for life’s “unexpected twists and turns”.

For example, if you’re carrying your mortgage into retirement and expect to sell up and downsize to clear the debt, you need to think about what to do if you change your mind and want to stay in your home, she says.

“It can be exactly what people need to make their mortgage more affordable, but they need to appreciate the wider implications.”

For homeowners like Shane it may be a gamble, but for him it’s a risk worth taking right now.

Additional reporting by Bernadette McCague.

Ways to make your mortgage more affordable

- Make overpayments. If you still have some time on a low fixed-rate deal, you might be able to pay more now to save later.

- Move to an interest-only mortgage. It can keep your monthly payments affordable although you won’t be paying off the debt accrued when purchasing your house.

- Extend the life of your mortgage. The typical mortgage term is 25 years, but 30 and even 40-year terms are now available.

[ad_2]

Source link